New York’s Climate Leadership and Community Protection Act (Climate Act) has a legal mandate for New York State greenhouse gas emissions to meet the ambitious net-zero goal by 2050. The Climate Action Council is responsible for preparing the Scoping Plan that will “achieve the State’s bold clean energy and climate agenda” and voted to release the Draft Scoping Plan late last year. I recently posted an article describing my fruitless search for cost number documentation that would enable me or anyone else to evaluate their cost claims. This post describes an egregious example of hiding the true costs of the Scoping Plan.

I have written extensively on implementation of the Climate Act because I believe the ambitions for a zero-emissions economy outstrip available renewable technology such that it will adversely affect reliability and affordability, risk safety, affect lifestyles, will have worse impacts on the environment than the purported effects of climate change in New York, and cannot measurably affect global warming when implemented. The opinions expressed in this post do not reflect the position of any of my previous employers or any other company I have been associated with, these comments are mine alone.

Background

The Climate Act establishes a “Net Zero” target by 2050. The Climate Act requires the Climate Action Council to “[e]valuate, using the best available economic models, emission estimation techniques and other scientific methods, the total potential costs and potential economic and non-economic benefits of the plan for reducing greenhouse gases, and make such evaluation publicly available” in the Scoping Plan. Starting in the Fall of 2020 seven advisory panels developed recommended strategies to meet the targets that were presented to the Climate Action Council in the spring of 2021. Those recommendations were translated into specific policy options in an integration analysis by the New York State Energy Research and Development Authority (NYSERDA) and its consultants. The integration analysis was used to develop the Draft Scoping Plan that was released for public comment on December 30, 2021. The public comment period extends through at least the end of April 2022.

I have been working my way through the massive draft document preparing comments on issues that I see. I have assessed the claimed benefits which was relatively easy because there was a relatively adequate amount of documentation. However, the cost documentation is very poor. I have explained that the only description of the net direct costs is a bar chart without a breakdown of the cost components. This article addresses a nuance to the net direct costs presented in the Draft Scoping Plan.

Net Direct Cost Information

In my latest assessment of direct costs in the Draft Scoping Plan I documented what information was provided for stakeholder assessment of costs. Starting on page 80 the Draft Scoping Plan section 10.3 Key Benefit-Cost Assessment Findings describes costs. However, the technical documentation is in Appendix G: Integration Analysis Technical Supplement. On page 64 of Appendix G, Section I, the text describes the cost metrics included in the Draft Scoping Plan:

The integration analysis includes calculations for three different cost metrics: Net Present Value (NPV) of net direct costs, annual net direct costs, and system expenditure.

-

-

-

- NPV of Net Direct Costs: NPV of levelized costs in each scenario incremental to the Reference Case from 2020-2050. All NPV calculations assume a discount rate of 3.6%. This metric includes incremental direct capital investment, operating expenses, and fuel expenditures.

- Annual Net Direct Costs: Net direct costs are levelized costs in a given scenario incremental to the Reference Case for a single year snapshot. This metric includes incremental direct capital investment, operating expenses, and fuel expenditures.

- System Expenditure: System expenditure is an estimate of absolute direct costs (not relative to Reference Case). Estimates of system expenditure do not reflect direct costs in some sectors that are represented with incremental costs only. These include investments in industry, agriculture, waste, forestry, and non-road transportation.

-

-

In my article I explained that the net direct costs represent the total costs of all the mitigation actions minus all the costs of a reference case. Appendix G notes that “redirecting investment away from status quo energy expenditures and toward decarbonization is key to realizing the aims of the Climate Act” but that overlooks that their estimate of status quo expenditures is already $2.7 trillion. At the time I found no discussion what was included in the $2.7 trillion estimate.

Draft Scoping Plan that Describes the Reference Case

In order to better understand what is included in the reference case I looked for the term. This section lists the results of a word search of the Draft Scoping Plan document for the term “reference case”. In the main body of text there were some references but the substantive information was in Appendix G.

Appendix G, Section I page 8 and 83:

Together, the benefits of avoiding economic impacts of damages caused by climate change and the improvements in public health total $400 – 420 billion. Realizing these benefits will require an incremental investment over the 30-year transition of approximately 10 percent in additional spending, or $290 – $310 billion, in addition to redirecting the approximately $2.7 trillion in expected system spending under the reference case towards New York’s low carbon future.

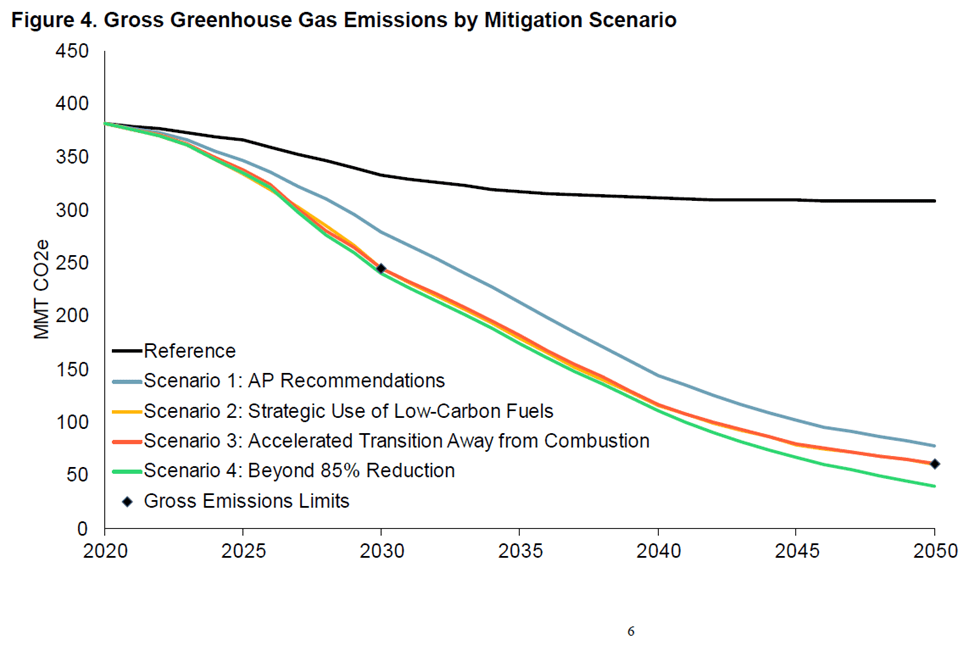

Appendix G, Section I page 12 there is a footnote for Figure 4: Gross Greenhouse Gas Emissions by Mitigation Scenario, without any accompanying text, presumably the caption for the figure.

6 The Reference Case is used for evaluating incremental societal costs and benefits of GHG emissions mitigation. The Reference Case includes a business as usual forecast plus implemented policies, including but not limited to federal appliance standards, energy efficiency achieved by funded programs (Housing and Community Renewal, New York Power Authority, Department of Public Service, Long Island Power Authority, NYSERDA Clean Energy Fund), funded building electrification, national Corporate Average Fuel Economy standards, a statewide Zero-emission vehicle mandate, and a statewide Clean Energy Standard including technology carveouts. For more details see Chapter 5.3.

Appendix G, Section I page 66:

When viewed in from a systems expenditure perspective (Figure 48), the NPV of net direct costs for Scenarios 2, 3, and 4 are moderate, ranging from 11-12% as a share of the NPV of reference case system expenditures ($2.7 trillion). Because significant infrastructure investment will be needed to maintain business as usual infrastructure within the state irrespective of further climate policy, redirecting investment away from status quo energy expenditures and toward decarbonization is key to realizing the aims of the Climate Act.

Appendix G, Section I page 68:

Net direct costs are measured relative to the Reference Case, but system expenditures are evaluated on an absolute basis. System expenditures increase over time as New York invests in infrastructure and clean fuels to meet Climate Act emissions limits. As a share of overall system expenditures, costs are moderate: 9-11% in 2030 and 25-26% in 2050 relative to current estimated expenditure levels.

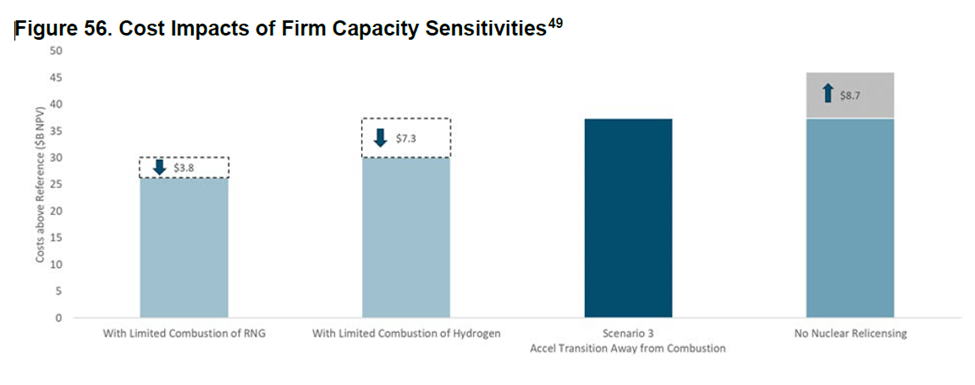

Appendix G, Section I page 76 in the title to Figure 56 there is a reference to footnote 49:

49 The costs presented represent the costs relative to a Reference Case with equivalent levels of electrification loads, and as a result are not directly comparable to the electric sector costs presented in the economy-wide analysis, in which costs are measured relative to a Reference Case with Reference loads.

Aside from similar statements on pages page 78, and 83 of Appendix G, Section I that is all the results for the search on “reference case”.

Discussion

One of the arguments in the discussion of costs and benefits is that the realizing these costs only represents an “incremental investment over the 30-year transition of approximately 10 percent in additional spending, or $290 – $310 billion, in addition to redirecting the approximately $2.7 trillion in expected system spending under the reference case”. In my original analysis of these costs, I mentioned that it is important to understand exactly what is included in the reference case in order to accept this statement. However, no explanation is prominently featured in documentation.

However, when I searched the document for the term “reference case” there was some information, buried in a footnote reference to a figure caption that was missing. It states that “The Reference Case includes a business as usual forecast plus implemented policies, including but not limited to federal appliance standards, energy efficiency achieved by funded programs (Housing and Community Renewal, New York Power Authority, Department of Public Service, Long Island Power Authority, NYSERDA Clean Energy Fund), funded building electrification, national Corporate Average Fuel Economy standards, a statewide Zero-emission vehicle mandate, and a statewide Clean Energy Standard including technology carveouts.” This exposes the scam. Cynic that I am I suspect that someone, somewhere intended to completely delete the caption for this figure so that the damning footnote would not be available.

Why is this so egregious? Recall that the presented net direct costs are relative to the reference case. If the reference case costs are higher by including mitigation efforts that are required to meet the Climate Act targets this approach perverts the numbers presented. Energy efficiency is a critical component of the mitigation strategies and this statement says we are going to include those costs in the reference case. Electrification of buildings is another key component and “funded building electrification” costs are in the reference case. The last two items take the cake however. The authors of the Integration Analysis have slipped the costs for the statewide zero-emissions mandate and Clean Energy Standard into the reference case so that those costs do not show up as net direct costs of the Climate Act.

If this is on the up and up then the projected benefits, which are also allegedly relative to the reference case, should exclude the emission reductions and associated benefits for energy efficiency programs and building electrification that are already funded, the statewide zero-emissions mandate, and the Clean Energy Standard. That may be the case but it is impossible to tell because the only numerical description of the net direct costs is a bar chart without a breakdown of the cost components.

Conclusion

I certainly could have mis-interpreted these numbers and normally when my evaluation shows significant differences from someone else’s work that is my first thought. However, this finding fits a consistent pattern of over-estimated benefits and under-estimated costs in the Integration Analysis.

The claimed benefits for the avoided cost of GHG emissions range between $235 and $250 billion, but I have shown that the Integration Analysis incorrectly calculates avoided GHG emissions benefits by applying the value of an emission reduction multiple times. If that error is corrected then the total benefits range from negative $74.5 to negative $49.5 billion.

It is very difficult to verify Draft Scoping Plan cost numbers because of the lack of documentation, but in two instances I have projected costs inconsistent with the Plan. I evaluated the projected costs for residential retrofits to electric heating. I estimated in the Draft Scoping Plan the entire building sector component cost is $230 billion relative to the reference case. I calculated that just the residential retrofit heat electrification costs range between $259 billion and $370 billion using one methodology and between $295 billion and $370 billion using a different methodology. In the other analysis I estimated the costs and benefits of upgraded rail transportation. The draft scoping plan claims a reduction of 200 million light duty vehicle miles at a per unit cost of $6 per mile or $1.2 billion between Scenarios 2 and 3 and Scenario 4. I estimate that the only valid cost for the difference between the scenario rail alternatives is $8.4 billion and that it would only provide a vehicle mile reduction of 64.7 million miles.

Were it not for this consistent pattern I would be reluctant to label this egregious example of hiding the true costs of the Scoping Plan as a deliberate attempt to obfuscate direct costs. However, the lack of documentation, the complete absence of reference case details and contrived way they present the cost numbers convinces me that this is deliberate. In order to “prove” that the Climate Act benefits out-weigh the costs they have deliberately cooked the books.

The rebuttal for my claim is for the Climate Action Council to provide complete and transparent documentation. It would be best if the Council would host an expert analysis session where the costing methodology used could be explained and the public could be given the opportunity to provide questions beforehand. Obviously, this post could provide a number of those questions. While it would not be possible to address all the sectors in such a session this format could provide answers to the cost projections most impactful to New York residents. Residential electrification and personal transportation head that list.

There is a massive disconnect between the costs projected in the Draft Scoping Plan any by other authors. Earlier this year I compared costs estimated in the Scoping Plan with costs in an article by Ken Gregory that is a critique of a report by Thomas Tanton “Cost of Electrification: A State-by-State Analysis and Results”. Tanton estimated that the New York overnight cost for a net-zero economy is $1.465 trillion. Gregory’s estimate for net-zero consistent with the Climate Act is $18.2 trillion. Until such time that the Climate Action Council produces documentation that enable independent verification of their estimates, I believe the actual costs will be consistent with these higher estimates.

7 thoughts on “Scoping Plan Cost Obfuscation”