On April 29, 2026, the Regional Greenhouse Gas Initiative (RGGI) states released a statement that Virginia was rejoining the program. On May 8, the RGGI states issued a notice that they were monitoring the allowance market in response to a sharp increase in the secondary futures market price. In a recent article I described the financial impact. This article addresses compliance.

Dealing with the RGGI regulatory and political landscapes is challenging enough that affected entities seldom see value in speaking out about fundamental issues associated with the program. I have been involved in the RGGI program process since its inception and have no such restrictions when writing about the details of the RGGI program. I have worked on every cap-and-trade program affecting electric generating facilities in New York including RGGI, the Acid Rain Program, and several Nitrogen Oxide programs, since the inception of those programs. I also participated in RGGI Auction 41 successfully winning allowances and holding them for several years. The opinions expressed in this post do not reflect the position of any of my previous employers or any other organization I have been associated with, these comments are mine alone.

RGGI is a market-based program to reduce greenhouse gas emissions from the power sector. It has been a cooperative effort among Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New York, Rhode Island, and Vermont since 2008, with New Jersey rejoining in 2020 and Virginia scheduled to rejoin beginning July 1, 2026; Pennsylvania recently decided not to join.

According to the RGGI program description, the states issue permits to emit a ton of CO₂ or allowances that are distributed almost entirely through regional auctions, and the proceeds are then reinvested in strategic energy and consumer programs. Those investments include energy efficiency, clean and renewable energy, beneficial electrification, greenhouse gas abatement and climate adaptation, and direct bill assistance, with energy efficiency receiving the largest share.

In a recent article I explained that the cost of RGGI allowances obtained at auction is not the only cost to consumers. In New York’s de-regulated market, the cost to purchase the allowances is embedded in the price bid by RGGI program fossil-fired power plants in the New York Independent System Operator (NYISO) energy auction. The NYISO chooses the power plants that will run based on the economic dispatch clearing price. When a RGGI-affected generating unit sets the price, all the generating units providing power get paid for the added cost of RGGI even though many do not have compliance obligations. I showed that this more than doubles the cost of compliance or more depending on the cost of allowances, making the cost an important affordability consideration.

RGGI allowance costs are driven by basic economic considerations. When there is scarcity, prices increase; when there is uncertainty about scarcity, costs also go up. The difference is that price increases associated with uncertainty can drop when more information is available, whereas if the RGGI plans for reducing the emission cap are unrealistic that bakes in scarcity so prices will increase structurally. When RGGI announced that Virginia was going to rejoin the program there was a market price spike based on a lack of information.

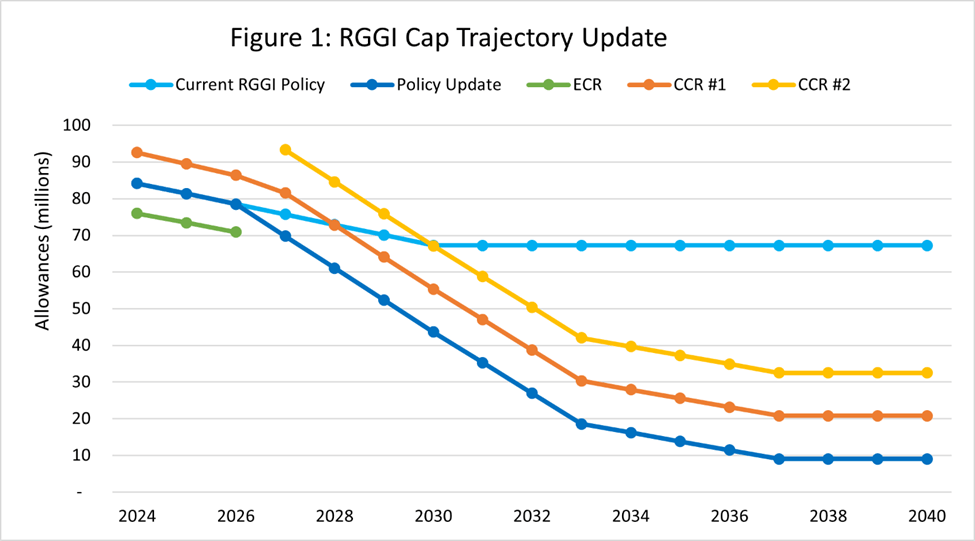

RGGI Cap Trajectory

The RGGI webpage describing last summer’s changes to the program included a graph that compares the current regional base cap (light blue) with the updated cap trajectory (dark blue). The orange and yellow lines display the total updated regional cap if all allowances are released from the updated first and second Cost Containment Reserve (CCR) tiers, respectively. The CCR tiers were added to reduce allowance costs. The bottom line is that the changes reduce the regional emissions cap in 2027 to 69,806,919 tons of CO2 from 75,717,784 tons under the previous Model Rule and then reduces allowances Allowances decline by approximately 10.5% of the 2025 budget, thereafter through 2033.

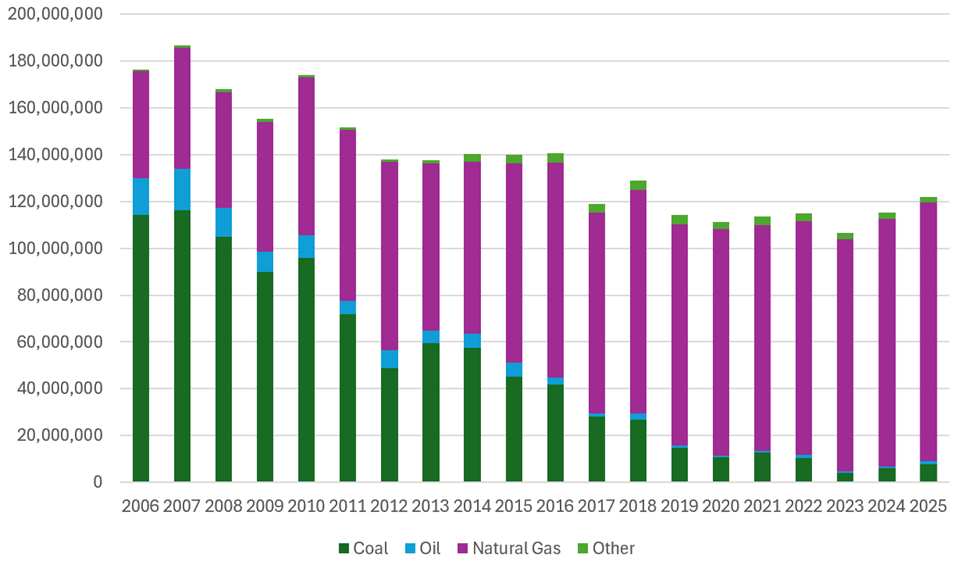

The RGGI emission cap trajectory was designed to be consistent with state net-zero targets. However, that trajectory is unrealistic. Figure 2 plots CO₂ emissions by fuel type across all eleven states from 2006 to 2025. What you see is fuel switching caused the reductions and that there are only minor opportunities for future fuel switching. When I analyzed the 2023 RGGI investment proceeds report, I estimated that only about 7.6% of observed emission reductions could be attributed to RGGI‑funded projects despite RGGI auction proceeds of over $7 billion since 2021. Changes to Federal policy, supply chain issues, and inflation coupled with load growth all indicate that reductions from other programs are unlikely as well. The cap trajectory is simply incompatible with reality.

Figure 2: Eleven State RGGI CO₂ Emissions (short tons) for all Programs 2006–2025

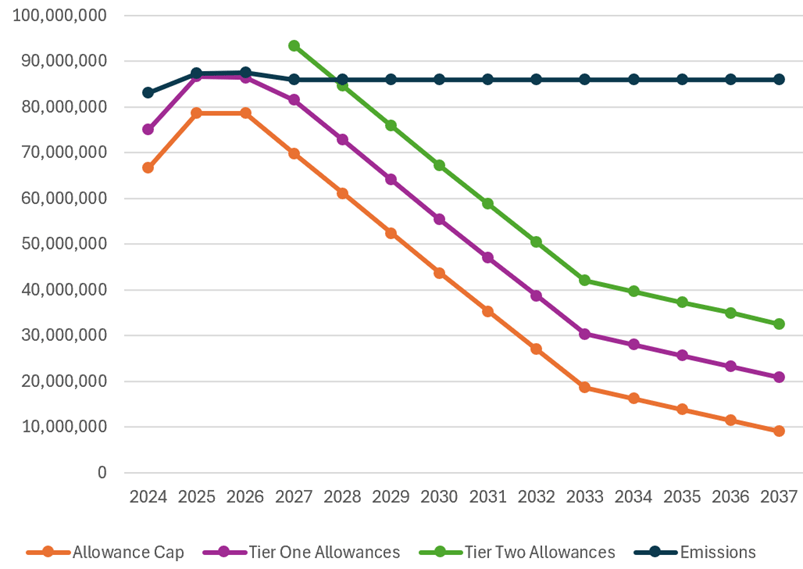

To determine when the allowances will run out it is necessary to consider emissions and the allowance trajectory. For this analysis I assume that future emissions equal the average of the last three years. In Figure 3, I plotted the updated cap trajectory (orange), total updated regional cap if all allowances are released from CCR Tier 1 (purple), CCR Tier 2 (green) and emissions in grey. I assume that allowance prices will exceed the trigger for the CCR allowance release every year. Note that in 2028 the emissions become greater than the allowances added to the market without Virginia in RGGI.

Figure 3: RGGI Emissions and Cap Trajectories for RGGI States Without Virginia

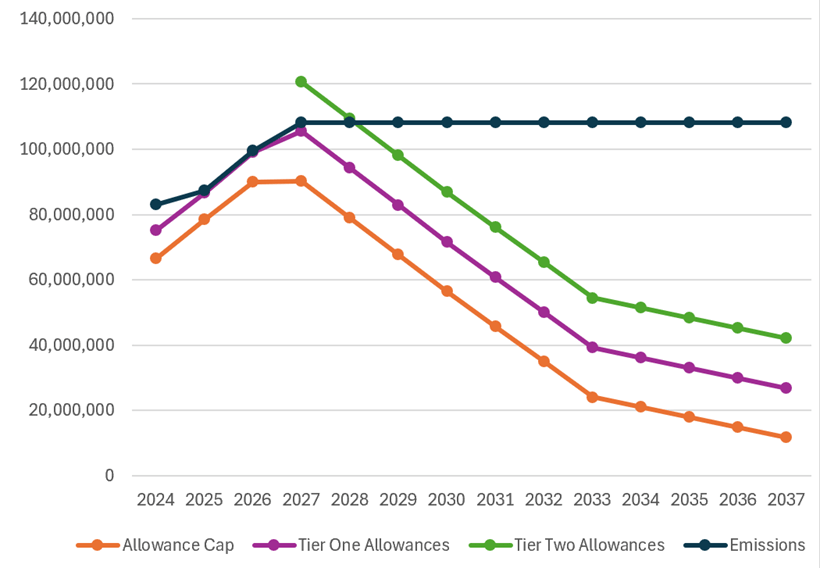

Figure 4 provides similar information with Virginia added to RGGI. There is no appreciable change to the time when the allowance allocations are less than the emissions so I believe that the addition of Virginia will not affect impacts.

Figure 4: RGGI Emissions and Cap Trajectories for RGGI States With Virginia

Allowance Bank

Comparing the allowance allocations to the emissions does not consider the allowances already in the system. The “allowance bank” is the aggregate number of allowances in circulation that have been issued but not yet surrendered for compliance (i.e., held in accounts or set‑asides). The original distribution of RGGI allowances was before the fracking revolution made natural gas a cost-effective substitute for replacing oil and coal generating units. When power plants switched to lower-emitting natural gas, much larger reductions in emissions than expected occurred and the allowance bank grew so large that the RGGI States implemented several adjustments to the allowances allocated to reduce the bank. These adjustments ended in 2025.

To refine when emissions could exceed the allowances available it is necessary to account for the allowance bank. RGGI does not provide a report that describes the status of the allowance bank, so I had to develop my own estimate.

Potomac Economics provides independent market monitoring analysis of RGGI that provide the information needed to estimate the bank. The Quarterly Reports on the Secondary Market are released several week after the end of a quarter. The Quarter 4 2025 report includes a description of CO2 allowance holdings:

CO2 Allowance Holdings – At the end of the fourth quarter of 2025:

- There were 175 million CO2 allowances in circulation.

- Compliance-oriented entities held approximately 125 million of the allowances in circulation (71 percent).

- Approximately 142 million of the allowances in circulation (81 percent) are believed to be held for compliance purposes.

Quarterly Allowance Status

The allowance bank is simply the difference between allowances being added and emissions that subtract allowances. Allowance transactions occur on a quarterly basis. Allowances are added at each auction and the annual true-up when allowances are surrendered to account for emissions occurs in the first quarter following the end of the year.

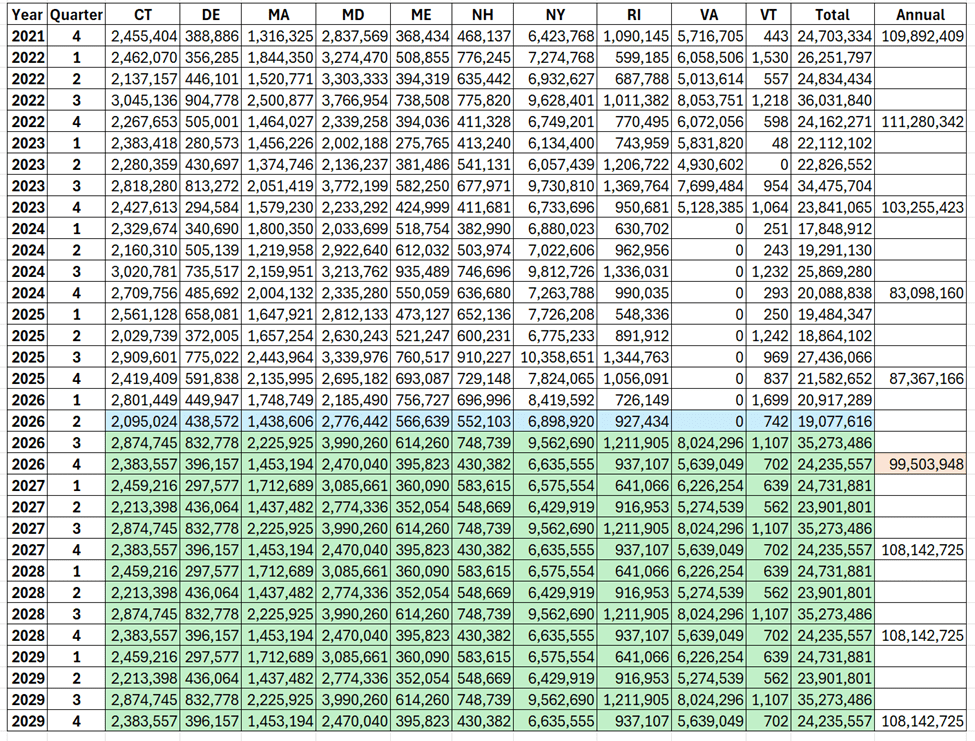

Emissions are used to reduce the allowance bank. Historical quarterly emissions are available on the RGGI COATS platform. Table 1 lists historical and projected CO2 emissions by state starting in quarter 4 2021 and ending in 2029. Historical emissions are not highlighted. For the second quarter of 2026 (highlighted in blue) I assumed that emissions would equal the average of the last two years. Starting in the third quarter of 2026 I assumed that emissions would equal the average of the three years when Virginia was part of RGGI. This is supported by Figure 2 that shows emissions have been relatively level since 2019 for the eleven states now in RGGI. The annual emissions are simply the sum of the four quarters. The 2026 total highlighted because it represents a mix of observed and projected emissions.

Table 1: RGGI Quarterly CO2 Mass Emissions (short tons)

The allowance bank is the balance of allowances awarded and surrendered. Figure 4 described the projected allowance distribution that was used to project future annual allowance distributions. I assume that all the CCR Tier 1 and Tier 2 allocations will be awarded in the first quarter and the remaining allowances distributed by the same amount each quarter. The Virginia allowance distribution has not been announced so I assume that they will be awarded in proportion to the control period when Virginia was a member.

The purpose of this analysis is to determine when the allowances in circulation are less than the emissions. The quarterly number of allowances in circulation is equal to the sum of the previous quarter allowances in circulation and the allowances awarded with allowances surrendered subtracted. Allowances are surrendered annually but I subtracted the emissions on a quarterly basis to get finer resolution.

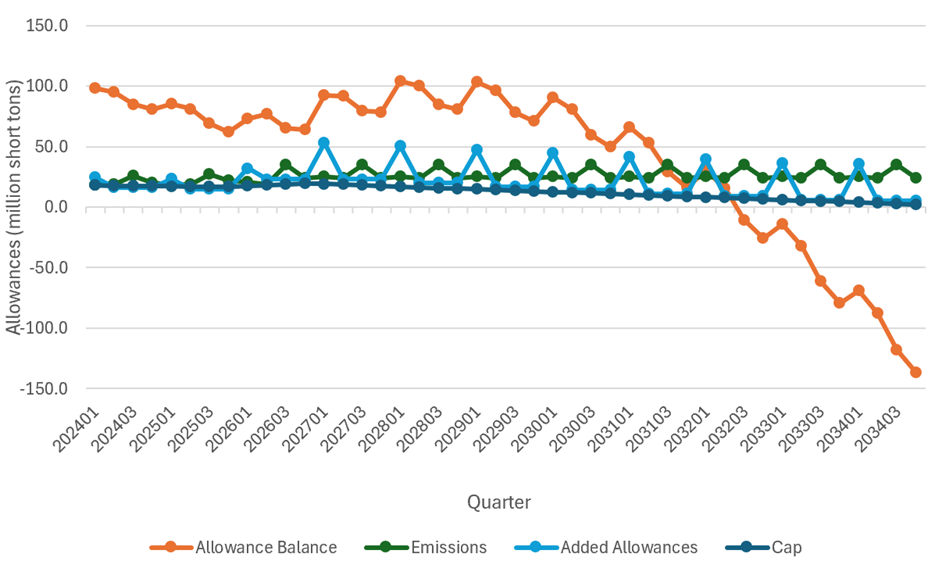

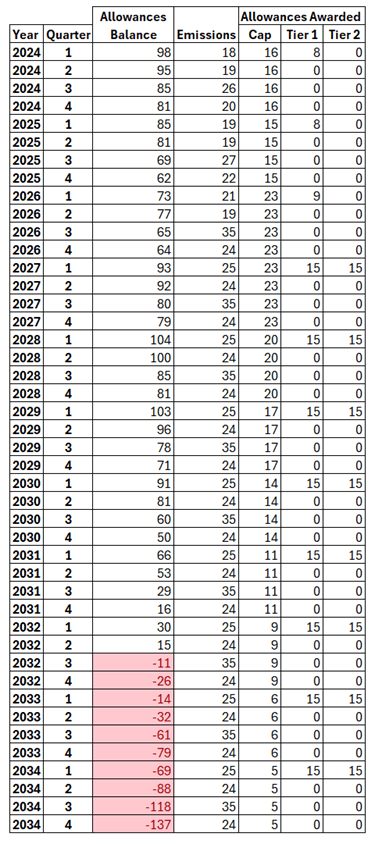

Figure 5 plots the quarterly emissions (green), allowance cap (dark blue), added allowances (light blue) and allowance balance (orange). This analysis assumes that emissions remain constant and shows that as the allowance cap is reduced the bank of allowances eventually is exhausted. When the allowance balance is less than zero there are no longer sufficient permits to emit CO2 and affected units must shut down or end up out of compliance. Table 2 lists the balances and shows that during the third quarter of 2032 there are insufficient allowances.

Figure 5: Quarterly RGGI Allowance Balance, Emissions and Allowance Cap

Table 2: Quarterly RGGI Allowance Balance, Added Allowances and Emissions

Discussion

To sum up, RGGI allowances necessary for facilities to operate will run out in the third quarter of 2033 if emissions remain constant and that the share of Virginia allowance allocations remains proportional to the period when Virginia was in RGGI. Note, however, that the market will be so tight in 2033 that some facilities will run out sooner. I would like to think that Virginia will remain consistent, but it is worrisome that Virginia decided to rejoin before the end of the current compliance period that ends this year. In the past states entered and left the program consistent with the three-year compliance period. If that decision was driven by an ideological desire to save the planet there is the possibility that a different allowance allotment will be used. If the Virginia allocations are proportional to the past the addition of the state will not markedly affect when the allowances run out.

This analysis does not try to distinguish between allowances held by compliance entities and those without compliance obligations. At the end of the fourth quarter of 2025 the Quarter 4 2025 report on the secondary market stated that “Approximately 142 million of the allowances in circulation (81 percent) are believed to be held for compliance purposes.” There are two implications. RGGI states have always assumed that the remaining 19% of the allowances are held for investment purposes and would eventually be used for compliance. Given that facilities need those allowances to operate it will be a seller’s market and prices should skyrocket when they are needed. There is another possibility. Some of those allowances could be held by organizations that want to prevent CO2 emissions and may not sell them at any price. In that case, the market will run out of allowances sooner.

On May 8, the RGGI states announced that they were aware of the short-term volatility associated with the announcement that Virginia would rejoin RGGI:

Recent futures prices are above thresholds established to automatically mitigate price growth by releasing additional allowances at auctions for cost containment. RGGI has a long history of stability. Regular program reviews have made adjustments to align the program with policy objectives of a reliable, affordable, and clean electricity supply. A sustained period of elevated auction prices would not meet these objectives and may require renewed consideration of improvements.

These results indicate that renewed consideration of the program design is necessary now to prevent sustained elevated auction prices.

Conclusion

For years the sources affected by RGGI and me have been warning that RGGI is headed to the point where there are insufficient allowances to enable sources to run and remain in compliance. If left unchecked this will lead to an artificial energy storage, The allowance cap trajectory is simply incompatible with observed and likely generating resource development that can displace existing resources. When RGGI announced that Virginia would rejoin the program, futures prices nearly doubled and the spot market price also spiked. Cost impacts will be evident before the allowances run out because scarcity will drive allowance prices higher because the present regulations bake in scarcity.

All politicians in RGGI states who are worried about energy affordability should seriously consider dropping out of the program because it is simply unaffordable and risky without major changes.