The Climate Leadership and Community Protection Act (Climate Act) establishes a “Net Zero” target by 2050 and the Draft Scoping Plan defines how to “achieve the State’s bold clean energy and climate agenda”. It is the right of every New Yorker to know how the agenda will affect affordability and reliability. This post documents my fruitless search for the cost number documentation that would enable me or anyone else to evaluate their cost claims.

I have written extensively on implementation of the Climate Act because I believe the ambitions for a zero-emissions economy outstrip available technology such that it will adversely affect reliability and affordability, risk safety, affect lifestyles, will have worse impacts on the environment than the purported effects of climate change in New York, and cannot measurably affect global warming when implemented. The opinions expressed in this post do not reflect the position of any of my previous employers or any other company I have been associated with, these comments are mine alone.

Background

The Climate Action Council is responsible for preparing the Scoping Plan that will “achieve the State’s bold clean energy and climate agenda”. The Climate Act requires the Climate Action Council to “[e]valuate, using the best available economic models, emission estimation techniques and other scientific methods, the total potential costs and potential economic and non-economic benefits of the plan for reducing greenhouse gases, and make such evaluation publicly available” in the Scoping Plan. Starting in the fall of 2020 seven advisory panels developed recommended strategies to meet the targets that were presented to the Climate Action Council in the spring of 2021. Those recommendations were translated into specific policy options in an integration analysis by the New York State Energy Research and Development Authority (NYSERDA) and its consultants. The integration analysis was used to develop the Draft Scoping Plan that was released for public comment on December 30, 2021. This draft includes results from the integration analysis on the benefits and costs to achieve the Climate Act goals. The public comment period extends through at least the end of April 2022, and will also include a minimum of six public hearings. The Council will consider the feedback received as it continues to “discuss and deliberate on the topics in the Draft” as it works towards a final Scoping Plan for release by January 1, 2023.

The Climate Action Council claims that the integration analysis was developed to estimate the economy-wide benefits, costs, and GHG emissions reductions associated with pathways that achieve the Climate Act greenhouse gas emission limits and carbon neutrality goal. It incorporates and builds from Advisory Panel and Working Group recommendations, as well as inputs and insights from complementary analyses, to model and assess multiple mitigation scenarios. In addition, there is historical/archived information is available through the Support Studies section of the Climate Resources webpage, and can found as part of the Pathways to Deep Decarbonization in New York State – Final Report.

During the development of the Draft Scoping Plan, consumer affordability was a major Climate Action Council feedback topic of discussion. The Draft Scoping Plan provides societal net direct costs but does not provide any consumer costs. The leader of the Integration Analysis effort at NYSERDA is Carl Mas. At 17:45 of the Climate Action Council meeting recording where this issue was debated, he explained that they were able to analyze for the technologies and the system changes in the scenarios to determine incremental cost to society.

In order to determine the actual costs to society you need to have specificity to distribute those costs. Is it going to be a ratepayer program? It is going to be a tax credit or incentive? How much is the Federal government going to weigh in to help buy down some of the cost. Without those types of programmatic specifics, we can’t actually analyze how much individual parts of our society should pay.

He went on to claim that: “It is really important to have articulated what the incremental costs would be and what the benefit cost analysis is, which is that we’ve done.” He concluded at 18:37 that:

I hope people don’t walk away thinking that waiting for implementation means that somehow there is kind of a done deal at that point. I mean, at that point is when we see the specific policy proposals that flow from a scoping plan. That’s when we can continue to debate and discuss how we implement these proposals.

Draft Scoping Plan Documentation

The purpose of this post is to document what information was provided for stakeholder assessment of costs. Starting on page 80 the Draft Scoping Plan section 10.3 Key Benefit-Cost Assessment Findings describes costs. However, the technical documentation is in Appendix G: Integration Analysis Technical Supplement and two spreadsheets:

- Appendix G: Annex 1: Inputs and Assumptions [XLSX]

- Appendix G: Annex 2: Key Drivers and Outputs [XLSX]

The following section lists all references to “direct costs” in the Appendix G text with some clarifying additions and my indented and italicized comments.

Page 61: Estimated system expenditures do not reflect direct costs in some sectors that are represented with incremental costs only. These include investments in industry, agriculture, waste, forestry, and non-road transportation.

No comment

Pages 64-68: Integration Analysis Costs

This whole section is included because it is the primary documentation source.

The integration analysis includes calculations for three different cost metrics: Net Present Value (NPV) of net direct costs, annual net direct costs, and system expenditure.

- NPV of Net Direct Costs: NPV of levelized costs in each scenario incremental to the Reference Case from 2020-2050. All NPV calculations assume a discount rate of 3.6%. This metric includes incremental direct capital investment, operating expenses, and fuel expenditures.

- Annual Net Direct Costs: Net direct costs are levelized costs in a given scenario incremental to the Reference Case for a single year snapshot. This metric includes incremental direct capital investment, operating expenses, and fuel expenditures.

- System Expenditure: System expenditure is an estimate of absolute direct costs (not relative to Reference Case). Estimates of system expenditure do not reflect direct costs in some sectors that are represented with incremental costs only. These include investments in industry, agriculture, waste, forestry, and non-road transportation.

I don’t have the appropriate background, so cannot speak to the calculation choices for these different cost metrics. However, I have been unable to find any numerical documentation (e.g., spreadsheets) that support the estimated cost metric expenditures.

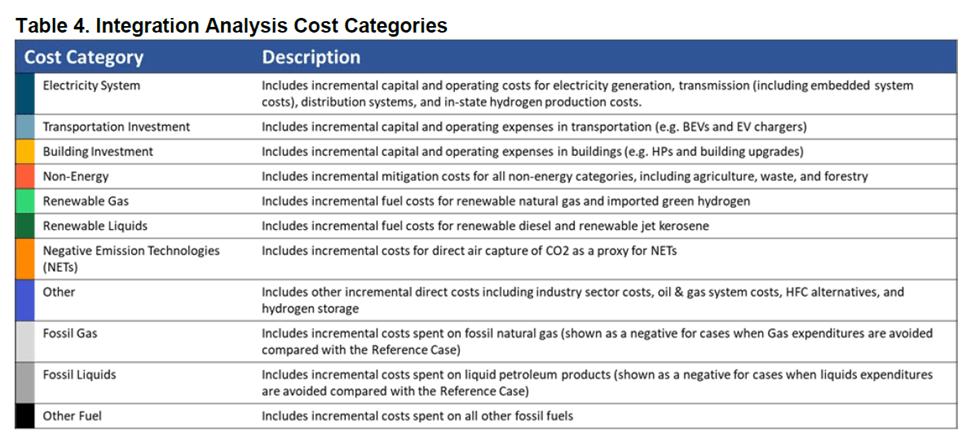

Cost categories included in the metrics listed above are shown in Table 4.

The spreadsheet Annex G: Inputs and Assumptions lists some of these costs and some of the assumptions made for these categories.

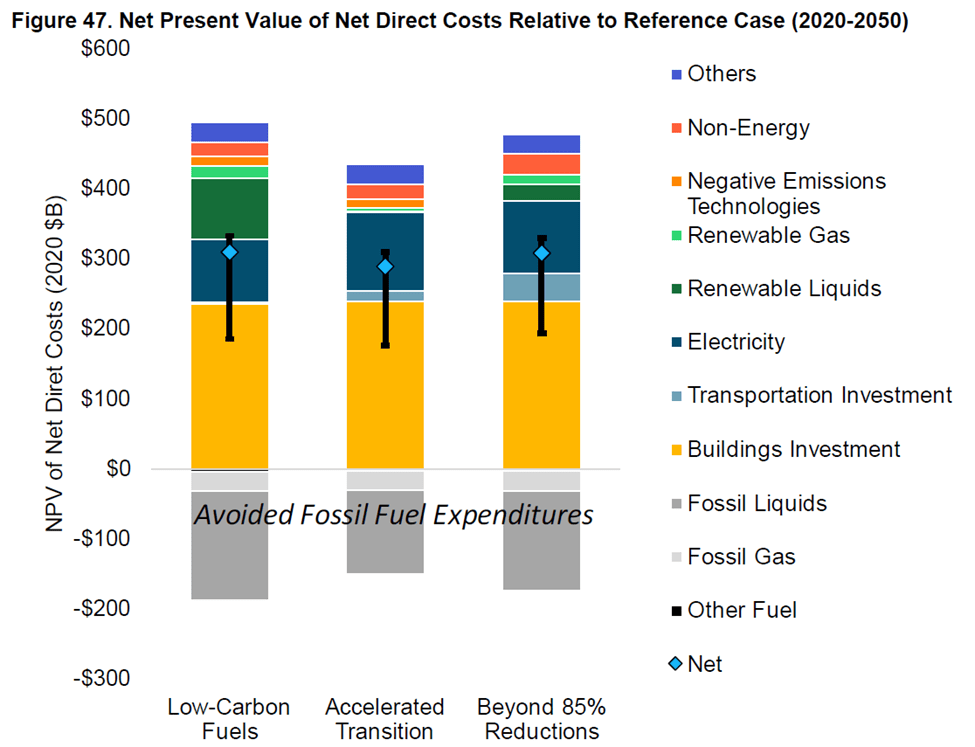

The NPV of net direct costs in Scenarios 2, 3, and 4 are in the same range given uncertainty and are primarily driven by investments in buildings and the electricity system (Figure 47). All scenarios show avoided fossil fuel expenditures due to efficiency and fuel-switching relative to the Reference Case (shown in the chart as negative costs). Scenario 2: Strategic Use of Low-Carbon Fuels includes significant investment in renewable diesel, renewable jet kerosene, and renewable natural gas. Scenario 3: Accelerated Transition Away from Combustion meets emissions limits with greater levels of electrification, which results in greater investments in building retrofits, zero-emission vehicles, and the electricity system. Scenario 4: Beyond 85% Reductions includes additional investment in transportation (rail, aviation, VMT reductions) and methane mitigation, and mitigates the need to invest in any negative emissions technologies. Scenario costs are sensitive to the price of fossil fuels and technology cost projections, as reflected in error bars.

In order to provide meaningful comments on these estimates much more information is needed. At an absolute minimum there should be a table that lists the values of the components of the Figure 47 bar charts. The Appendix G spreadsheet annexes document many of the figures in the Scoping Plan but none of the figures with direct costs are documented.

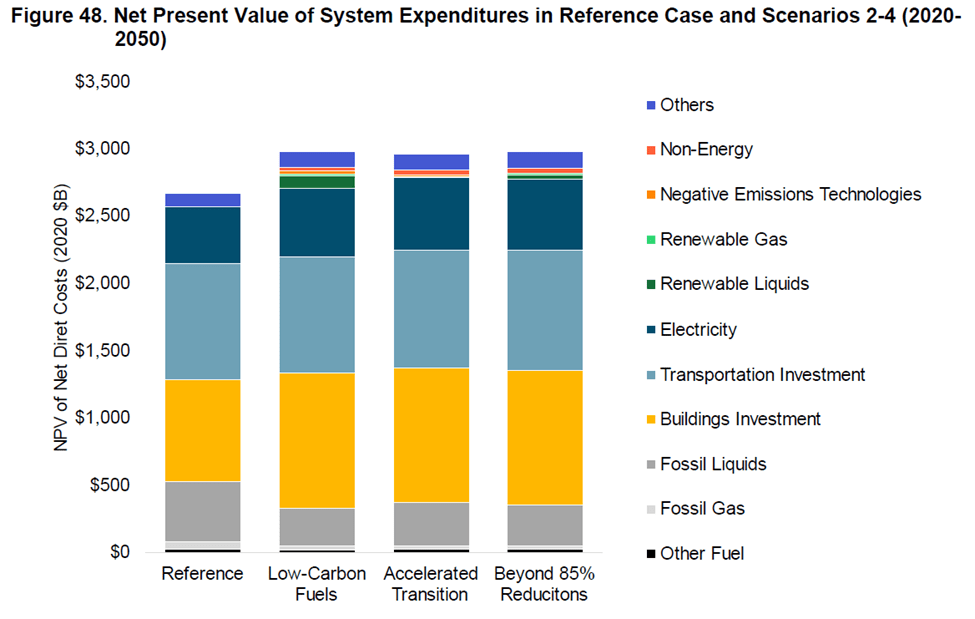

When viewed in from a systems expenditure perspective (Figure 48), the NPV of net direct costs for Scenarios 2, 3, and 4 are moderate, ranging from 11-12% as a share of the NPV of reference case system expenditures ($2.7 trillion). Because significant infrastructure investment will be needed to maintain business as usual infrastructure within the state irrespective of further climate policy, redirecting investment away from status quo energy expenditures and toward decarbonization is key to realizing the aims of the Climate Act.

Not only are the Draft Scoping Plan Integration Analysis cost calculations undocumented but there is mis-leading reporting as in this paragraph. These numbers represent the total costs of all their mitigation actions minus all the costs of a reference case. The statement “redirecting investment away from status quo energy expenditures and toward decarbonization is key to realizing the aims of the Climate Act” overlooks their estimate that status quo expenditures are already $2.7 trillion. There is no discussion whether that $2.7 trillion only represents current consumer costs or includes additional infrastructure spending. I expect that investments above and beyond what consumers are already are paying are needed so the actual consumer costs are being understated by this way of presenting the societal costs.

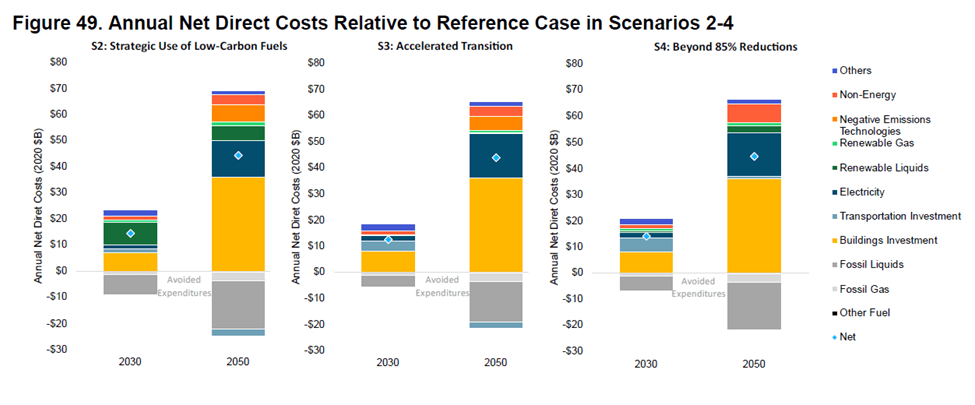

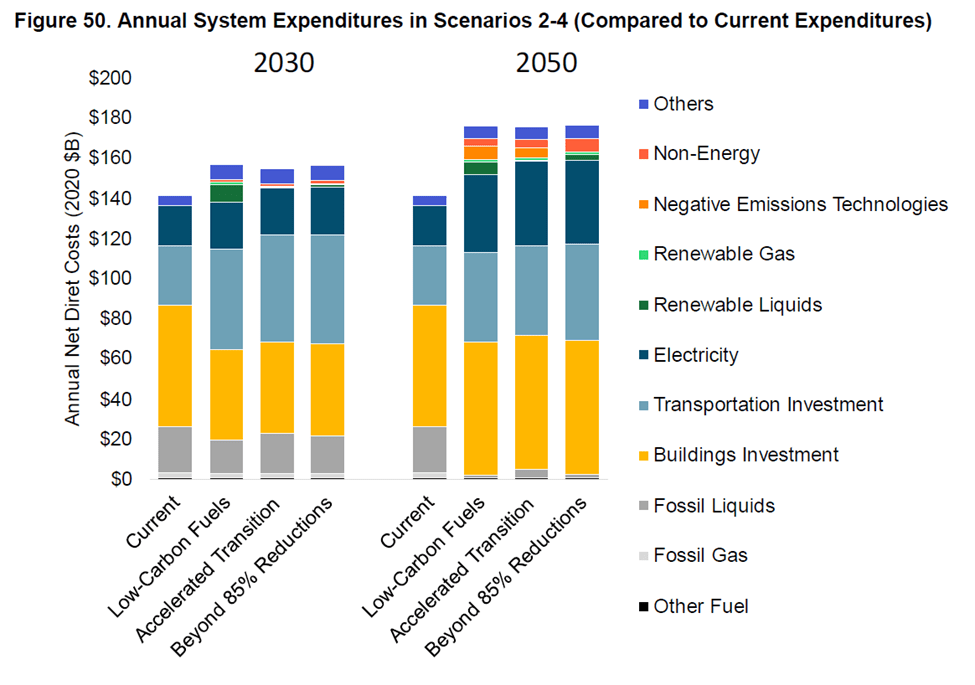

Annual net direct costs show the timing of key investments required to meet Climate Act emissions limits. Scenario 2 includes significant investment in renewable diesel, renewable jet kerosene, and renewable natural gas starting in the mid-2020s. Scenario 3 includes greater levels of electrification compared to Scenario 2, which results in greater investments in building retrofits, zero-emission vehicles, and the electricity system. Scenario 4 layers on even further investments in transportation and non-energy mitigation than Scenario 3 and includes a targeted investment in low-carbon renewable fuels, although not as intensive as that in Scenario 2. Both Scenarios 2 and 3 include investment in negative emissions technologies (NETs) to achieve net zero emissions by 2050, while Scenario 4 does not require any NETs to meet carbon neutrality by 2050. In 2030, annual net direct costs are on the order of $15 billion per year, approximately 0.6% of GSP; in 2050, costs increase to $45 billion per year, or roughly 1.4% of GSP.

This represents the description of the cost differences between the three scenarios. In order to provide full documentation, all the numbers associated with the assumptions used to derive the numbers have to be presented and they don’t even list the component numbers of the bar charts. For example, consider NETs. Obviously, the final cost needs to be presented but we also need to know the costs per type of negative technology, the control efficiency expected, the number of these magical technology systems that do not exist at commercial scale that will be needed, and the assumed location assume for them because all those factors affect cost. I could find no reference to these technologies in the Appendix G appendices. Moreover, I have been unable to find the necessary documentation for any of the technologies proposed for the mitigation scenarios at a level where it is possible to provide meaningful comments.

Net direct costs are measured relative to the Reference Case, but system expenditures are evaluated on an absolute basis. System expenditures increase over time as New York invests in infrastructure and clean fuels to meet Climate Act emissions limits. As a share of overall system expenditures, costs are moderate: 9-11% in 2030 and 25-26% in 2050 relative to current estimated expenditure levels.

This figure also demonstrates the need for more information for meaningful comments. If the current system expenditures were documented then we could understand what is incorporated in their numbers. It would also be possible to verify their approach by comparing their estimates to other sources of data. It might also be possible to figure out whether their reference estimated expenditure costs represent increases to current levels?

Page 70: Benefit-Cost Findings

- Net direct costs are small relative to the size of New York’s economy. Net direct costs are estimated to be 0.6-0.7% of GSP in 2030, and 1.4% in 2050.

No comment

Page 70: 3.5 Uncertainty and Sensitivity Analysis

There also are references to “direct cost” associated with the following figures in this section:

- Figure 52. NPV of Net Benefit of Mitigation Scenarios (2020-2050): Range Including Uncertainty in Fuel Cost, Technology Cost

- Figure 53. NPV of Scenario Net Direct Costs: Fuel cost sensitivity for Scenarios 2 through 4 For biofuels

- Figure 54. NPV of Scenario Net Direct Costs: Biofuel cost sensitivity for Scenarios 2 through 4

- Figure 55. NPV of Scenario Net Direct Costs: Technology cost sensitivity

This represents the Integration Analysis information that is supposed to address the concerns I raised here. Clearly without complete documentation it is impossible to agree or disagree that these cost sensitivities are complete or accurate.

Integration Analysis Documentation

The Integration Analysis technical documentation is in Appendix G: Integration Analysis Technical Supplement and two spreadsheets:

- Appendix G: Annex 1: Inputs and Assumptions [XLSX]

- Appendix G: Annex 2: Key Drivers and Outputs [XLSX]

This section describes the cost information provided in these spreadsheets.

As noted previously, neither spreadsheet documents the numbers presented in Figures 45-55 in Appendix G: Integration Analysis Technical Supplement. In addition, there is insufficient information to determine how the numbers were calculated. Some of the assumed technology costs are included but there are gaps in either information or methodology that prevent replication of the values presented. Consequently, it is impossible to provide substantive comments on the costs claimed.

Conclusion

The Climate Act requires the Climate Action Council to “[e]valuate, using the best available economic models, emission estimation techniques and other scientific methods, the total potential costs and potential economic and non-economic benefits of the plan for reducing greenhouse gases, and make such evaluation publicly available” in the Scoping Plan (my emphasis added). The fact that the only description of the net direct cost is a bar chart without a breakdown of the cost components clearly demonstrates that this Climate Act requirement has been ignored in the Draft Scoping Plan.

If it were not so important for the future of New York State it would be tempting to laugh at the coverup of the numbers. Unfortunately based on everything I have seen the coverup is deliberate because the projected costs are extremely high. This is an inevitable result as shown in the United Kingdom where “the press seems to have finally woken up to the huge damage already being wreaked on the country, all as a result of successive governments’ climate policies”. It is almost as if the authors of the Draft Scoping Plan are hoping to get the plan approved before the public catches on.

In the absence of sufficient publicly available information to evaluate the cost projections, New Yorkers are expected to trust these numbers. I was able to evaluate the Draft Scoping Plan benefit numbers to verify whether trust is warranted. The Draft Scoping Plan claims that “The cost of inaction exceeds the cost of action by more than $90 billion.” I have shown that the Integration Analysis incorrectly calculates avoided GHG emissions benefits by applying the value of an emission reduction multiple times. If only that error is corrected the total benefits range from negative $74.5 to negative $49.5 billion instead of net benefits ranging from $90 billion to $120 billion. I conclude that New Yorkers should not trust the cost values in the Draft Scoping Plan and that comments demanding adequate documentation be provided are appropriate.

4 thoughts on “Climate Act Scoping Plan Cost Documentation Failures”