On April 29, 2026 the Regional Greenhouse Gas Initiative (RGGI) states announced that Virigina was rejoining. The original intent of this post was to describe the potential impact of that development, but while doing research it became obvious that the bigger story is the impact of the cost adder for RGGI allowances on the electric market. On May 8, the RGGI states issued a notice that they were monitoring the allowance market in response to a sharp increase in the secondary futures market price so I am not the only one concerned about this development.

Dealing with the RGGI regulatory and political landscapes is challenging enough that affected entities seldom see value in speaking out about fundamental issues associated with the program. I have been involved in the RGGI program process since its inception and have no such restrictions when writing about the details of the RGGI program. I have worked on every cap-and-trade program affecting electric generating facilities in New York including RGGI, the Acid Rain Program, and several Nitrogen Oxide programs, since the inception of those programs. I also participated in RGGI Auction 41 successfully winning allowances and holding them for several years. The opinions expressed in this post do not reflect the position of any of my previous employers or any other organization I have been associated with.

Background

RGGI is a market-based program to reduce greenhouse gas emissions from the power sector(Factsheet). It has been a cooperative effort among Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New York, Rhode Island, and Vermont since 2008, with New Jersey rejoining in 2020 and Virginia scheduled to rejoin beginning July 1, 2026. Pennsylvania recently decided not to join.

According to the RGGI program description, the states issue CO2 allowances that are distributed almost entirely through regional auctions, and the proceeds are then reinvested in strategic energy and consumer programs. Those investments include energy efficiency, clean and renewable energy, beneficial electrification, greenhouse gas abatement and climate adaptation, and direct bill assistance, with energy efficiency receiving the largest share.

Virginia Rejoins RGGI

The RGGI Statement said that, with Governor Spanberger’s approval of Virginia’s regulation reinstating the state’s CO2 budget trading program, Virginia’s participation and compliance obligations will resume on July 1, 2026. Virginia’s allowance budget for the second half of 2026 will be 11.48 million allowances, and the state will participate in the September 9 and December 2, 2026 auctions. Virginia will also originate 1.148 million Cost Containment Reserve allowances for the remainder of 2026, and later this year the state will undertake regulatory action to align its program with the Third Program Review and the updated Model Rule by January 1, 2027.

Cost Impact of Virginia Rejoining RGGI

RGGI allowance costs are driven by basic economic considerations. When there is scarcity prices increase and when there is uncertainty about scarcity costs also go up. The difference is that price increases associated with uncertainty can drop when more information is available. Whereas it is possible that the RGGI plans for the emission cap are so aspirational that scarcity is baked in. A Perplexity AI review of the Annual RGGI Market Monitor reports describes observed price spikes were associated with the following:

- A regime change in supply (cap adjustment, Cost Containment Reserve (CCR) exhaustion, bank recalculation) alters the scarcity narrative and raises uncertainty.

- That uncertainty interacts with short‑term shocks—Clean Power Plan expectations and nuclear retirements in 2015, cap/bank adjustments in 2021, CCR exhaustion plus an expanded derivatives market in 2024, and the 2025 program review, the Virginia state election, and winter demand expectations in late 2025.

- A growing options and futures market means those shocks are transmitted and sometimes amplified via hedging and speculative flows, which shows up explicitly as higher option‑implied volatility in the RGGI monitor reports.

The price of RGGI allowance futures recently rose sharply after the announcement that Virginia would rejoin RGGI. There is no publicly available resource describing the price of allowances on the secondary market. Instead, subscription-based trade news services determine the secondary allowance prices. The Carbon Pulse article RGGI Market: Historic rally rages over 30% into new week as RGAs breach $40 description stated the following before the article contents were available only to subscribers:

Last week’s surge in RGGI Allowance (RGA) futures carried over into the new week as prices broke all-time highs above the $40 threshold, up more than 30% in the last three days, with traders telling Carbon Pulse it’s unclear where and when the current rally could reach a pinnacle.

RGGI Cost Impacts

Several NYISO market experts have pointed out to me that this is a serious issue that should be addressed. RGGI costs have two effects on customer supply costs: the direct cost of the allowances themselves for each generating unit and the impact of the cost adder used by generating units in their bid prices. After a long delay I finally have found time and agree that this needs to be discussed.

In a deregulated electric market such as that run by the New York Independent System Operator, power plants, load-serving entities, and other participants submit competing bids and offers to an auction that determines the least-cost set of resources needed to meet demand while respecting grid limits. NYISO’s day-ahead energy market is a financially binding, security-constrained auction in which generators, loads, and other participants submit bids and offers for each hour of the following day. NYISO then runs an optimization that selects the least-cost portfolio of resources from those bids that can reliably meet forecasted demand given transmission limits and unit constraints, and the resulting locational marginal prices are used for settlement.

A useful way to picture the market is as a stack of generator offers, with the cheapest megawatts at the bottom and progressively more expensive plants piled on top until the stack is high enough to meet NYISO forecast load. At that point, the most expensive marginal unit needed sets the clearing price for the zone. If the marginal unit must add a CO2 allowance cost to its bid, then the clearing price rises accordingly, increasing the price paid to all accepted generators in that market interval. Lower-emitting generators still incur their own allowance costs, but their revenues also increase because they are paid the higher clearing price, and non-emitting units receive the clearing-price increase as pure profit without any direct CO2 compliance cost.

RGGI Cost Estimate

To calculate the best estimate of the cost of RGGI on the New York electric system, it would be necessary to obtain hourly emissions and operating data for all units participating in the NYISO market. Unit-specific operating information is proprietary and not publicly available. For a first-cut estimate, emission monitoring data for RGGI program units were downloaded from the EPA CAMPD database for 2025. Those hourly data include CO2 emissions, heat input, and gross load, so estimates of heat rate and CO2 emission rate can be derived. However, this database was not designed specifically for heat-rate analysis, and the hourly values necessarily rely on simplifying assumptions about fuel heat content for emissions-trading purposes. Nonetheless, the data are indicative.

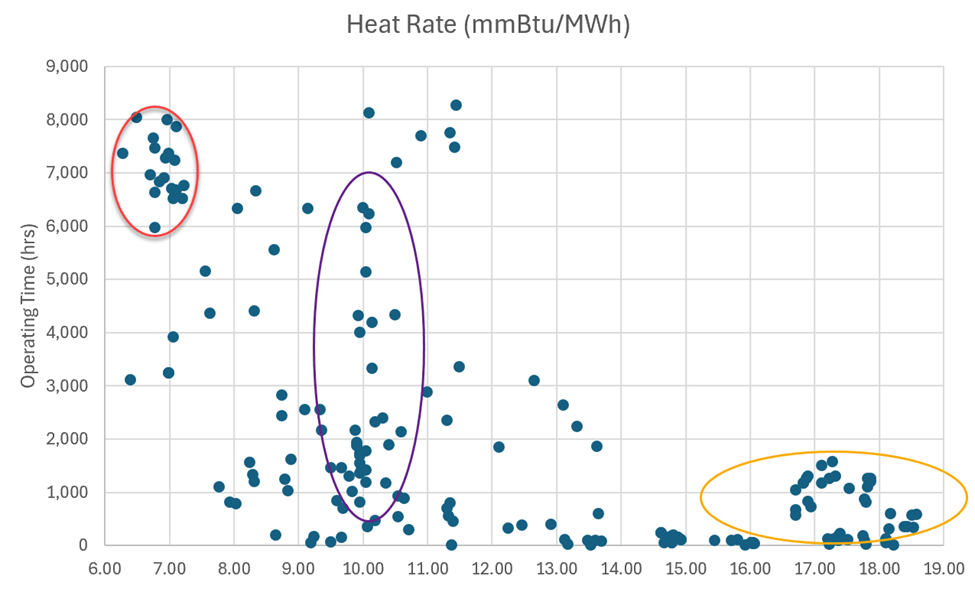

Figure 1 plots 2025 annual operating time against annual heat rate for New York RGGI units. It would be better to plot heat rate against capacity factor, but the EPA data do not include nameplate capacity in a form that can be readily matched to NYISO data. Three clusters stand out: highly efficient gas-fired combined-cycle units with low CO2 rates (red circle), steam boilers in the middle of the distribution (purple circle), and older simple-cycle turbines with the highest heat rates and CO2 emission rates (dark yellow circle).

Operating Time for NYS RGGI Units

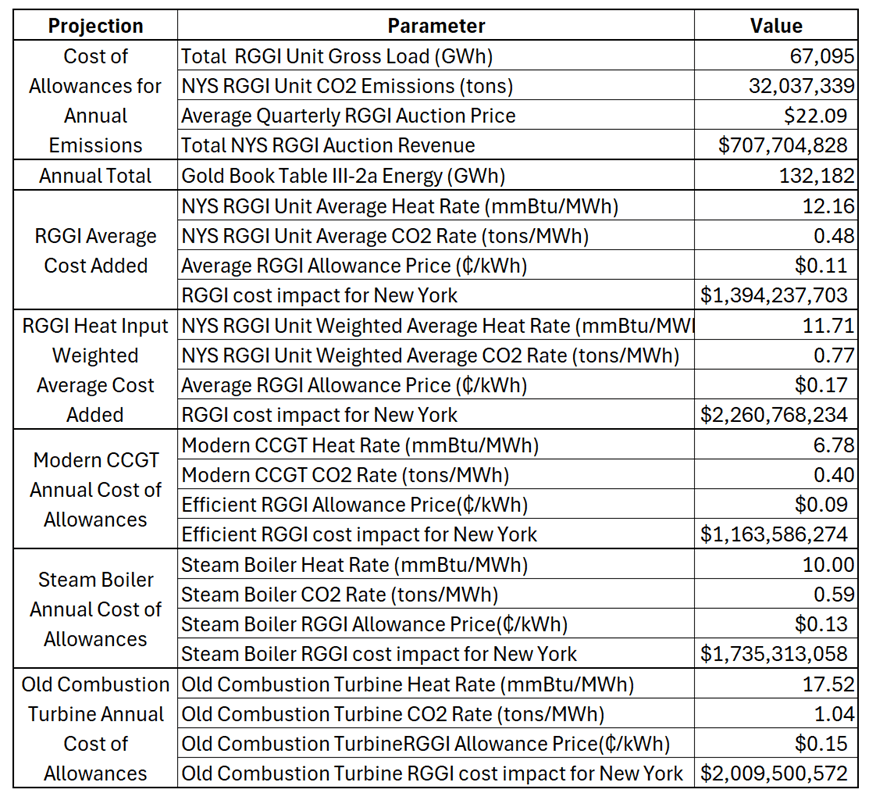

To illustrate the effect of the RGGI cost adder, the estimates below use annual values as a proxy for the hourly impacts that would ideally be summed across the year. In 2025, statewide gross energy from New York RGGI units totaled 67,094.6 GWh, those units emitted 32,037,339 tons of CO2, the average quarterly RGGI auction price was $22.09 per ton, and NYISO Gold Book Table III-2a reports total net New York energy of 132,182 GWh.

The direct cost of allowances alone can be estimated by multiplying annual emissions by the average auction price: 32,037,339 tons times $22.09 per ton, or about $707.7 million. That simple estimate does not account for the effect of the NYISO market clearing-price adder that is passed through to ratepayers.

Table 1 provides bounding estimates for that market effect. The first section, “Cost of Allowances for Annual Emissions,” documents the direct allowance-cost numbers just described. The Annual Total section lists the NYISO total net energy used in the scaling calculation. The remaining scenarios use observed heat rates and observed CO2 emission rates derived from EPA data to estimate an allowance-cost adder in dollars per MWh, which is then multiplied by total NYISO energy to estimate the statewide annual cost impact.

Table 1: 2025 New York State RGGI Unit Operating Characteristics & Emissions, RGGI Allowance Cost, and Consumer Cost Impacts

Using average 2025 data for New York RGGI units, the “RGGI Average” scenario yields an estimated statewide cost impact of $1.39 billion, nearly double the direct cost of purchasing allowances alone. Using the heat input weighted input data, the statewide cost impact would be $2.26 billion. If every fossil unit in New York were a modern state-of-the-art combined-cycle unit, represented here by the average of the Cricket Valley and Valley Energy Center units, the “Modern CCGT” scenario yields about $1.16 billion. A representative steam-boiler scenario yields about $1.74 billion. The worst-case “Old Combustion Turbine” scenario yields about $2.01 billion, although that result is not realistic because it would require an old combustion turbine to be marginal in every hour and every relevant zone.

Discussion

RGGI allowance prices raise the marginal bid of emitting generators in NYISO, so the allowance “cost adder” lifts the market clearing price on essentially all electricity consumed in New York, causing total costs to ratepayers that can be two or more times higher than the direct allowance expenditures and creating a windfall for non‑emitting “free‑rider” units. In simplest terms assuming that the weighted average heat rate is the marginal heat rate (11,700 mmBtu/MWh), the weighted average emission rate (0.77 tons/MWh), the last auction RGGI closing price ($22), and apply that allowance adder to all delivered MWh (150 TWh) shows that RGGI raises retail bills on the order of $2.26 billion dollars per year at the allowance cost in late March. The recent price spike doubled this cost increasing this impact of RGGI to $12.3 million a day. The generators’ direct compliance costs are much smaller, with the difference accruing as bonus money to non‑emitters. It is not yet clear whether the recent spike in RGGI allowance futures will be the new normal or whether it is the result of today’s uncertainty about the impact of Virginia rejoining RGGI.

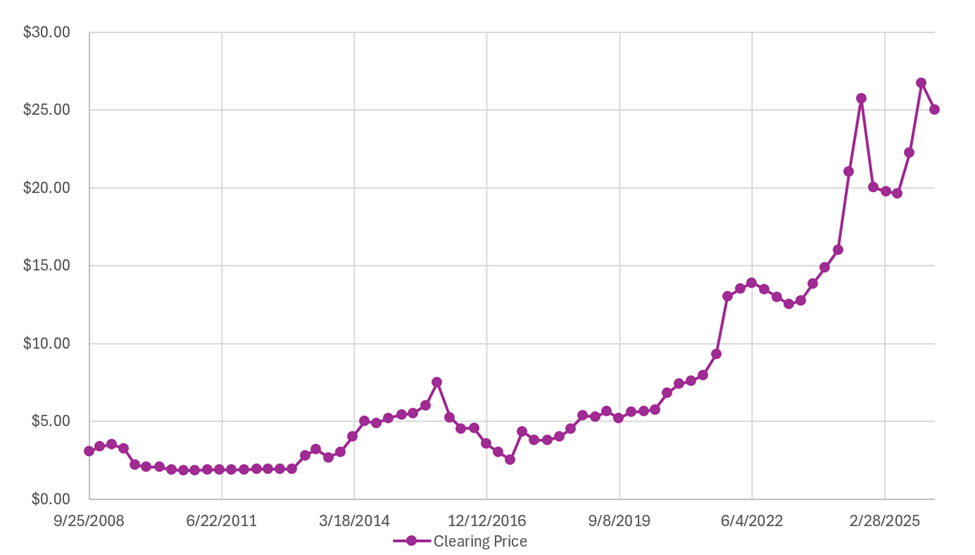

RGGI allowance prices from 2009 to 2018 were generally below $5 per ton, but since then both prices and volatility have increased materially (Figure 2). It is not yet clear whether the recent spike in RGGI allowance futures will be fully reflected in future auction prices. Importantly, when generating units incorporate the RGGI cost into their market bids they use the current spot market price. In other words, the impacts of this price spike are showing up in electric prices now. When the net monthly bills go out if this trend continues there will be a noticeable increase in costs.

Figure 2: RGGI Quarterly Auction Allowance Clearing Prices

Only the NYISO has the proprietary hourly market and unit-commitment information needed to estimate the total consumer impact of the RGGI cost adder with confidence. Even so, the bounding scenarios presented here indicate that the added cost to consumers is likely substantial and that a significant portion of that added cost appears as windfall revenue to lower-emitting and non-emitting generators.

The theory that auction revenues support cost-effective consumer benefits typically considers only the direct cost of allowances. Even if all the allowance auction proceeds were directly returned to customers this analysis shows that when the market-clearing-price effects of the RGGI allowance adder are included consumer impacts will be significant.

Conclusion

My market expert tutors pointed out that the RGGI carbon tax has been ignored for years. The ultimate beauty of the program is that the costs of RGGI allowances are not visible on electric bills because the allowance costs are buried in the bid prices. We are sure that the PSC would never allow any information about RGGI allowance costs to be included as information items on electric bills. Ultimately the best tax is a hidden tax.

This issue was reportedly a topic of conversation at NYISO during the early years of RGGI implementation. Given that allowance prices are now an order of magnitude higher than they were for many years and could go higher still, it is time for NYISO to reconsider the windfall profits that non-emitting units are reaping on the backs of New York ratepayers.

Roger, this is absolutely your best work. And that is saying something.

You are great ally.

LikeLike

Thank you. I had a lot of help with this one.

LikeLike