This is a follow up to my article published at Watts Up With That Resources for the Future: Retail Electricity Rates Under the Inflation Reduction Act of 2022 and re-published here. The article addressed the Resources for the Future (RFF) Issues Brief titled Retail Electricity Rates Under the Inflation Reduction Act of 2022 claim that the legislation, will “save typical American households up to $220 per year over the next decade and substantially reduce electricity price volatility.” I got a comment here that raised two flaws in my arguments. I used data from the United States Energy Information Administration (EIA) Electricity Data Browser for Texas to test the hypothesis that increased renewable energy resources would lower electricity costs. This article addresses the flaws raised.

The comment that exposed my flawed argument was provided by Dr. Michael Giberson, associate professor of practice in the Area of Energy, Economics, and Law with the Rawls College of Business at Texas Tech University. He commented that:

When I follow your directions for your chart using the EIA data you describe, I get a very different picture. Avg residential power prices in Texas peak in mid 2008, then fall for several years before coming up more recently. Your chart is showing something other than what you describe.

Further, inflation adjusted power prices have been falling over the 2001-2022 period. Using CPI data with January 2022 = 100, average real price in early 2001 was about 12.5 cents then jumped up to 18.5 cents in mid 2008 before falling back to about 12.5 cents in 2022.

I hypothesized that if I used the United States Energy Information Administration (EIA) Electricity Data Browser tool I could find data that showed that prices would go up in states where renewable energy development has increased the fraction of renewable energy generated and I used Texas an example. I downloaded the monthly total net generation (GWh) and the net generation from just renewable resources so I could calculate the percentage of renewable generation energy. Then I downloaded the average monthly residential average price of electricity.

I went back and reviewed my work and have to apologize to everyone because I mistakenly used the wrong monthly residential cost data. Dr. Giberson used the correct data as shown below. The Texas data do not illustrate any relationship between the percentage of monthly renewable energy generated per month (left axis) and the monthly residential electric price (right axis). What it does show is that the observed variability of the monthly prices is large in Texas.

Importantly, this result invalidates my hypothesis that these two parameters could be used to show that when the Texas electric system added more renewable energy the costs went up. Obviously, these data do not confirm that hypothesis. Upon further review in order to pick out a trend in the cost data I should have adjusted for inflation as Dr. Giberson suggested. The variation in the data before the renewable energy production kicked in also suggests that picking out a trend is more complicated than I thought it would be.

An alternative hypothesis is that this is an issue with just the Texas data so I did the same thing with California data. The results shown below are significantly different than Texas. There is less cost variability and the increase after 2005 is not as pronounced. It does appear that costs go up and renewable penetration goes up but I did not adjust for inflation to test that theory.

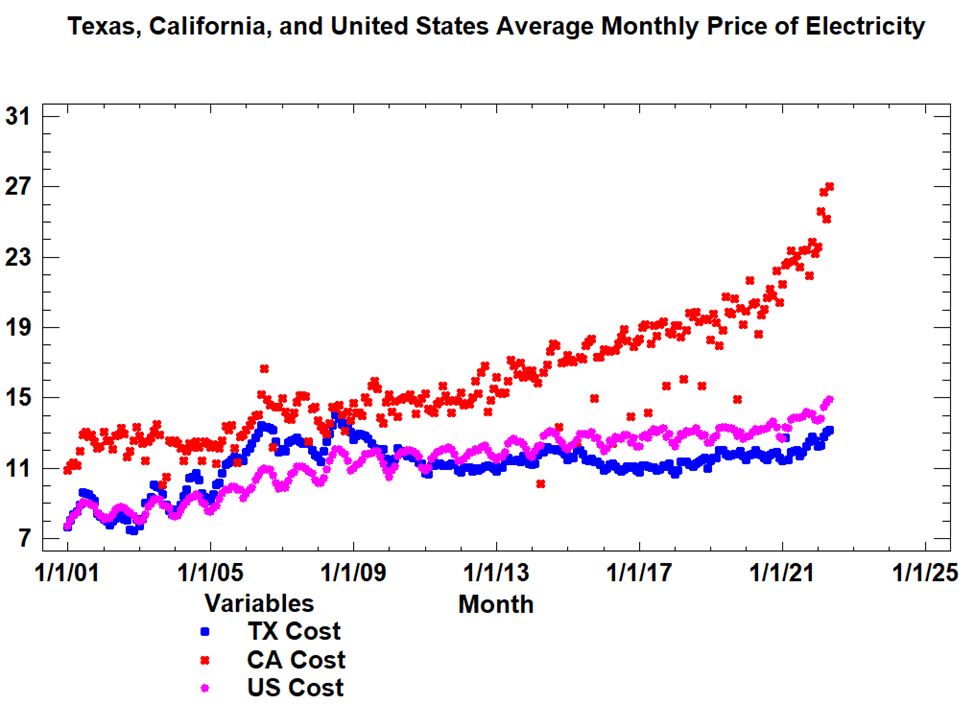

The axes in the Texas and California charts are different so inter-comparison is difficult. When combined the results are messy but there are a couple of interesting things. Texas residential electric costs are significantly lower (89% in 2021) and the spread has increased over time. However, during the years 2005 to 2009 the Texas energy costs were less than 20% lower apparently because something happened to the Texas market in that time. Dr. Giberson notes that the inflation adjusted real price in early 2001 was about 12.5 cents then jumped up to 18.5 cents in mid-2008 before falling back to about 12.5 cents in 2022. The other interesting point is that as the percentage of renewable generation increases the spread between the monthly values increases which I think reflects seasonal variations in resource availability.

I also extracted data for the United States as a whole. Note that US residential electric costs increased at the same time Texas rates increased after 2005. The same volatility increase as additional renewable power is added is apparent. It is notable that historically there has been a clear annual cycle of costs peaking in the summer and troughing out in the winter. With regards to the RFF cost projection, I don’t think there is much evidence that increasing renewable penetration has increased cost but the annual cycle appears to be becoming less pronounced. Of course, trying to analyze a trend when there was a pandemic is likely to end up with massive uncertainty.

As noted, there is one aspect that is consistent for all the renewable penetration data. As the percentage of renewable energy production increases the volatility of the monthly production increases. Wind resources are generally higher when there is a greater contrast in air masses in the spring and fall. Obviously solar resources are lower in the winter when days are shorter. I believe that there is an important outcome of that finding. The RFF brief claims that adding more renewable resources will “substantially reduce electricity price volatility”. I believe that the argument is that the price of fossil fuels is subject to many extraneous factors that affect price but those factors are smaller for renewable resources. I think these data suggest that the inherent variability in a weather-dependent source of power generation could increase electric price volatility as the system becomes more dependent upon those resources.

The following figure lists cost data for Texas. California, and the country as a whole. What interests me are the outliers. For example, in March 2014 the monthly residential price of electricity in California was 15.86 cents. It dropped to 10.12 cents in April then rebounded to 16.46 cents in May. Subsequent outliers are all either in October or April for the next five years. This might represent increased wind availability but it is not clear why it is not as pronounced before or after this period if that is the case.

More important are the high outliers. In California, the monthly price was 15.17 cents in June 2005, jumped to 16.65 cents in July, and then dropped to 14.89 cents in August. In Texas, the monthly price was 11.4 cents in January 2021, jumped to 12.74 cents in February, and then went down to 11.5 cents in March. The Texas blackout was the cause for the energy price spike in February 2021 but I don’t know of any specific problem in California in July 2005. I suspect that these events will become more common as renewable penetration increases but the data do not show that yet.

Conclusion

Obviously, I need to double check my data analyses before publishing. I found that using the correct data leads to an analysis that is consistent with every other aspect of the net-zero transition that I have looked at. Everything is more complicated than it appears at first glance and any conclusions drawn are more uncertain. Any claims about conclusive evidence should be regarded cynically.

The RFF Retail Electricity Rates Under the Inflation Reduction Act of 2022 issues brief claims that the legislation, will “save typical American households up to $220 per year over the next decade and substantially reduce electricity price volatility.” My original conclusion was that the Texas cost and renewable generation data showed that it was unlikely that there would be cost savings due to increased renewable energy but I used incorrect data. Using the correct data, I could argue that the Texas results did not show a decrease which is contrary to the RFF projection, but it is also reasonable to argue that were it not for the renewable generation that costs would have increased more than they did. At first glance and without adjusting for inflation, California data suggested that increased penetration of renewable resources increases costs but there are clear uncertainties that make this a tenuous conclusion.

Despite the problems with my analysis, I remain convinced that the RFF projection is unlikely. The models used for this kind of analysis do not do future changes to the electric system well. For example in the comments on my original post, Rud Istvan explained why wind renewables cannot reduce electricity prices. He showed that EIA LCOE estimates do not accurately project future costs for renewable energy development because they don’t include the costs to make the energy generated available when and where it is needed. Francis Menton recently made a persuasive argument that all projections for future electric systems overbuild the wind and solar resources resulting in higher costs. Worse, you still need a backup dispatchable resource and someone also has to provide ancillary services to maintain the grid’s ability to move power around. I believe that the modeling down by RFF and others does not adequately take those factors into account and if it did it would not show reduced costs.

One final point about the data. There is a real trend in the renewable energy generation data that needs to be watched in the future. All the data show that as the percentage of renewable energy production increases the volatility of the monthly production increases. The RFF brief claims that adding more renewable resources will “substantially reduce electricity price volatility”. While there is no apparent impact in retail costs due to this observed volatility in these data, I suspect that will change in the future.