The Climate Leadership and Community Protection Act (Climate Act) has a legal mandate for New York State greenhouse gas emissions to meet the ambitious net-zero goal by 2050. The scoping plan claims that “The cost of inaction exceeds the cost of action by more than $90 billion”. In my recent verbal comments at the Syracuse Climate Act public hearing I said that statement is inaccurate and misleading. This post consolidates documentation that has been presented in multiple earlier posts that supports my statement that the costs far exceed the benefits.

Everyone wants to do right by the environment to the extent that they can afford to and not be unduly burdened by the effects of environmental policies. I have written extensively on implementation of New York’s response to climate change because I believe the ambitions for a zero-emissions economy embodied in the Climate Act outstrip available renewable technology such that it will adversely affect reliability, impact affordability, risk safety, affect lifestyles, and will have worse impacts on the environment than the purported effects of climate change in New York. New York’s Greenhouse Gas (GHG) emissions are less than one half one percent of global emissions and since 1990 global GHG emissions have increased by more than one half a percent per year. Moreover, the reductions cannot measurably affect global warming when implemented. Bottom line for me is that in its present form the Climate Act will do more harm than good. The opinions expressed in this post do not reflect the position of any of my previous employers or any other company I have been associated with, these comments are mine alone.

Climate Act Background

The Climate Leadership and Community Protection Act (Climate Act) establishes a “Net Zero” target by 2050. The Climate Action Council is responsible for preparing the Draft Scoping Plan that defines how to “achieve the State’s bold clean energy and climate agenda”. They were assisted by Advisory Panels who developed and presented strategies to the meet the goals to the Council. Those strategies were used to develop the Integration Analysis prepared by the New York State Energy Research and Development Authority (NYSERDA) and its consultants that quantified the impact of the strategies. That analysis was used to develop the Draft Scoping Plan that was released for public comment on December 30, 2021.

Benefits Exceed the Costs Claim

The Draft Scoping Plan claim that “The cost of inaction exceeds the cost of action by more than $90 billion” is presented in Figure 51 in Appendix G Integration Analysis Technical Supplement. The Climate Act overview presentation for the public hearings included a similar figure and made the claim. However, there is a caveat or in this case, a trick. In the following figure I have highlighted the description that notes that the benefits are “relative to Reference Case”. By the way, that caveat is usually not noted when these results are presented.

Reference Case Costs

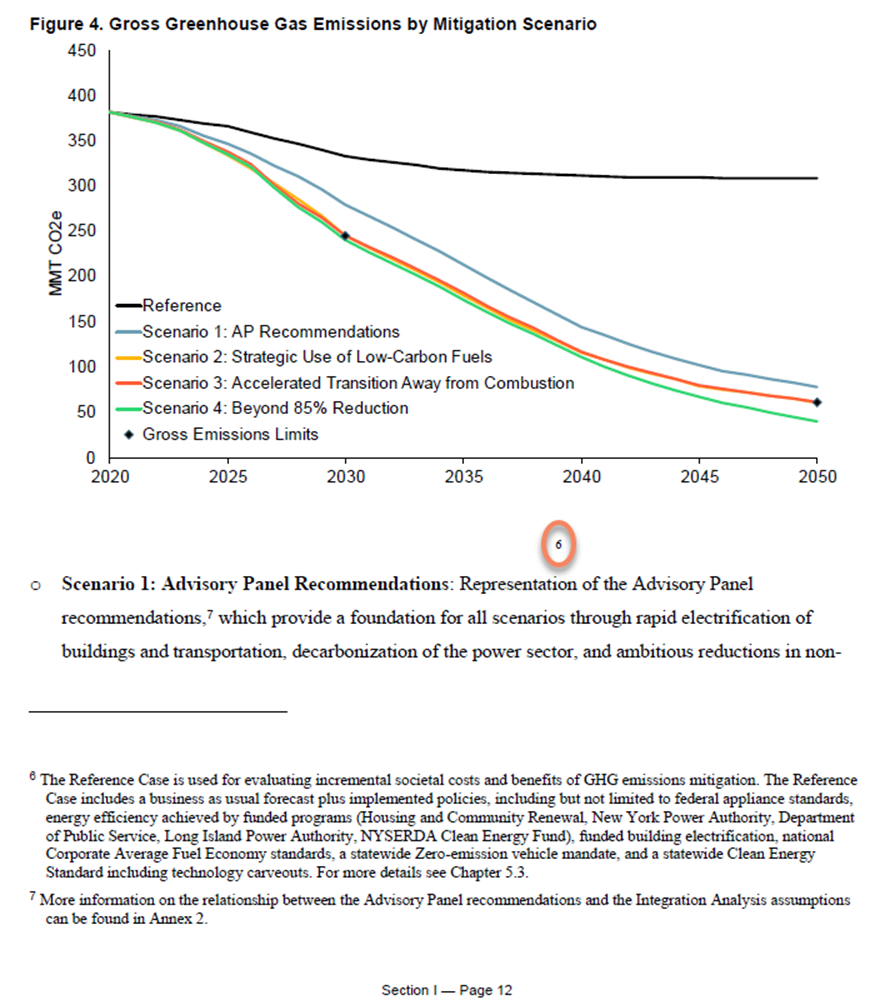

The important point is that the costs shown subtract the reference case costs from the costs attributed to the Climate Act. As a result, the control measures included in the Reference Case make all the difference in the claim. I did not pick up on this nuance for several months. When I did notice the qualifying statement, I started looking for Reference Case documentation in the Draft Scoping Plan. Ultimately, I ended up searching the document for the phrase “reference case. The following figure reproduces the page with the documentation on page 12 in Appendix G Integration Analysis Technical Supplement Section I. The documentation is buried in the footnote for the circled reference for the blank caption to Figure 4. Given its importance to this critical claim I can’t help but wonder why this important definition is buried.

The footnote text describes what is in the Reference Case. It includes a “business as usual” forecast plus implemented policies. The implemented policies include but are not limited to:

- Federal appliance standards

- Energy efficiency achieved by funded programs (Housing and Community Renewal, New York Power Authority, Department of Public Service, Long Island Power Authority, NYSERDA Clean Energy Fund)

- Funded building electrification

- National Corporate Average Fuel Economy standards

- Statewide Zero-emission vehicle mandate

- Statewide Clean Energy Standard including technology carveouts

The Climate Act requires the Climate Action Council to “[e]valuate, using the best available economic models, emission estimation techniques and other scientific methods, the total potential costs and potential economic and non-economic benefits of the plan for reducing greenhouse gases, and make such evaluation publicly available” in the Scoping Plan. In order to fulfill this obligation, I think the Draft Scoping Plan should describe all control measures, the expected costs for those measures and the expected emission reductions for the Reference Case, the Advisory Panel scenario and the three mitigation scenarios. While there is a large amount of information provided, this information is not available as far as I can tell. Particularly concerning is the complete lack of detailed cost information.

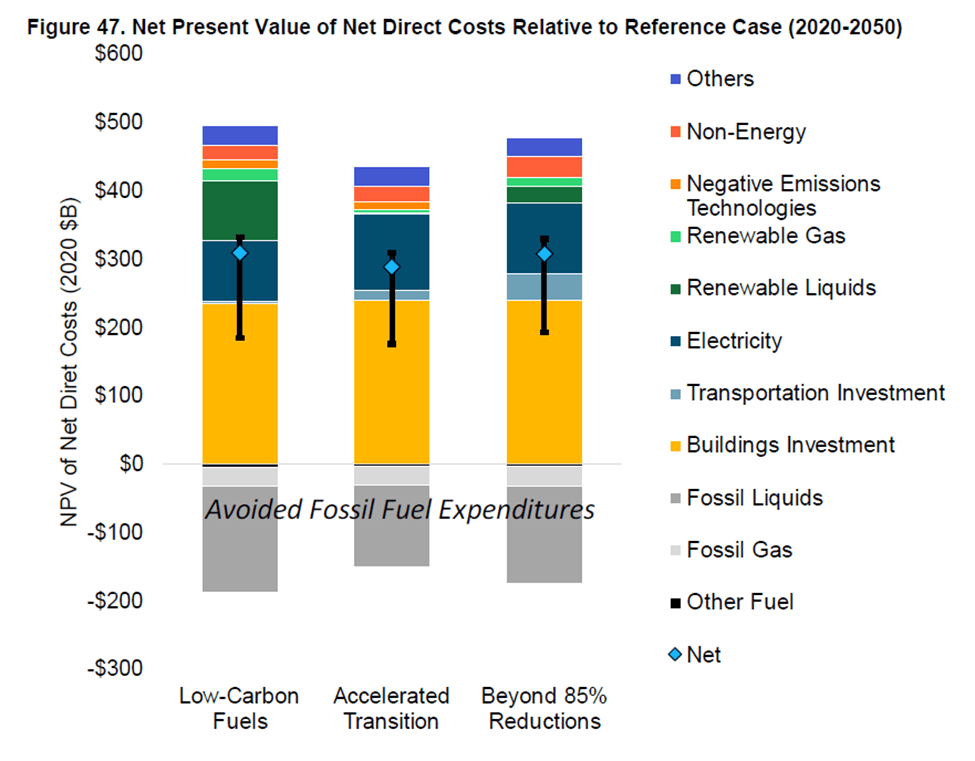

The total system expenditures are shown in Figure 48. The text notes that the reference case total is $2.7 trillion but that is the only quantified reference. I estimate that the mitigation scenarios are around $3 trillion making the costs relative to the reference case around $300 billion for the three mitigation scenarios. Also note that the values of the expenditure categories on the right are not listed so readers can only guess the values based on the size of the bars.

Figure 47 lists costs relative to Reference Case for the three mitigation scenarios. In other words, the numbers presented subtract out the Reference Case costs. The trick used to claim that the benefits are greater than the costs is to argue that significant costs that are needed to meet Climate Act targets are in programs that are already implemented. For example, consider transportation investments that I estimate total around $700 billion. There are two already implemented transportation investment programs in the Reference Case: national corporate average fuel economy standards and statewide zero-emission vehicle mandate. I accept that Federal fuel economy standards don’t represent a cost for the Climate Act. New York passed legislation setting a goal for all new passenger cars and trucks sold in New York State to be zero-emissions by 2035 in April 2021 so this is technically an already implemented program.

However, suggesting that the zero-emissions vehicle “implemented policy” should not be included in the Climate Act implementation costs is disingenuous at best. The press release announcing that the Governor signed the legislation states: “The actions announced today in advance of Climate Week 2021 support New York’s ambitious goal of reducing greenhouse gas emissions by 85 percent by 2050, as outlined in the Climate Leadership and Community Protection Act.” It goes on to quote Governor Hochul: “New York is implementing the nation’s most aggressive plan to reduce the greenhouse gas emissions affecting our climate and to reach our ambitious goals, we must reduce emissions from the transportation sector, currently the largest source of the state’s climate pollution”. I think that these statements pretty well represent any dispassionate observer’s belief that the only reason for this is mandate is to support the Climate Act. As such those costs are not legitimate Reference Case costs.

If the Draft Scoping Plan provided the costs for each of the control measures as I believe is appropriate, then it would be a simple matter to determine what the costs for Transportation Investments should be. Instead, I had to eyeball guess the size of the transportation investment bar in Figure 48 to be around $700 billion. While that total includes the costs for the Federal fuel economy standard, that has to be much smaller than all the costs associated with going to zero-emissions vehicles. There are about 10 million vehicles in the state so assuming that the Federal fuel economy standard will cost $7,000 per vehicle that means that the total cost is $70 billion and that zero-emissions vehicles cost $630 billion. As a result, the direct costs increase by $630 billion.

Avoided Cost of Carbon Benefits

In Figure 51 the costs are compared to benefits. As shown in Figure 46, the largest benefit comes from avoided GHG benefits. I believe there is an error in that calculation. Scoping Plan relies on flawed DEC Value of Avoided Carbon Guidance. The Guidance includes a recommendation to estimate emission reduction benefits for a plan or goal. I believe that the guidance approach is wrong because it applies the social cost multiple times for each ton reduced. I maintain that it is inappropriate to claim the benefits of an annual reduction of a ton of greenhouse gas over any lifetime or to compare it with avoided emissions. The social cost calculation that is the basis of the Scoping Plan carbon valuation sums projects benefits for every year for some unspecified lifetime subsequent to the year the reductions. As shown above, the value of carbon for an emission reduction is based on all the damages that occur from the year that ton of carbon is reduced out to 2300. Clearly, using cumulative values for this parameter is incorrect because it counts those values over and over. I contacted social cost of carbon expert Dr. Richard Tol about my interpretation of the use of lifetime savings and he confirmed that “The SCC should not be compared to life-time savings or life-time costs (unless the project life is one year)”.

Corrections to Figure 51 Net Present Value of Benefits and Costs

The following table corrects the issues described here. If we fix the misleading trick then the Draft Scoping Plan net system costs are increased by $630 billion. Correcting the multiple counting error drops the avoided GHG benefits estimate to $60 billion. The result is that the costs exceed the benefits by at least $690 billion.

There’s More

There is another issue associated with the claim that “The cost of inaction exceeds the cost of action by more than $90 billion”. As shown, there is a caveat that the comparison is relative to the Reference Case. I showed how the semantic justification that the transportation investments were already implemented excluded the costs of the zero-emissions vehicle mandate from the costs side of the comparison. In order to further tilt the results, the benefits attributed to the transportation investments were not excluded in the comparison. In other words, the comparison takes out the costs that would hurt their case but leaves in benefits that help make the case that the benefits are greater than the costs.

Conclusion

In my opinion the Climate Act story that the benefits out-weigh the costs is incorrect. I have shown how the trick to deceive the public works. If the Draft Scoping Plan described all the control measures, the expected costs for those measures and the expected emission reductions for the Reference Case, the Advisory Panel scenario and the three mitigation scenarios, then the public would be able to decide for themselves which costs associated with “already implemented” program are appropriate. The lack of documentation prevents that.

More detailed documentation information is available here and here.