The Regional Greenhouse Gas Initiative (RGGI) is a carbon dioxide control program in the Northeastern United States. One aspect of the program is a program review that is a “comprehensive, periodic review of their CO2 budget trading programs, to consider successes, impacts, and design elements”. This post described the comments I submitted on the third program review process that is underway.

I have been involved in the RGGI program process since its inception. I blog about the details of the RGGI program because very few seem to want to provide any criticisms of the program. RGGI is a market-based emissions market program similar to what has been proposed for the Climate Leadership & Community Protection Act (Climate Act. I have written over 300 articles about New York’s net-zero transition because I believe the ambitions for a zero-emissions economy embodied in the Climate Act outstrip available renewable technology such that the net-zero transition will do more harm than good. The opinions expressed in this post do not reflect the position of any of my previous employers or any other company I have been associated with, these comments are mine alone.

Background

RGGI is a market-based program to reduce greenhouse gas emissions. According to RGGI:

The Regional Greenhouse Gas Initiative (RGGI) is a cooperative effort among the states of Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Vermont, and Virginia to cap and reduce power sector CO2 emissions.

RGGI is composed of individual CO2 Budget Trading Programs in each participating state. Through independent regulations, based on the RGGI Model Rule, each state’s CO2 Budget Trading Program limits emissions of CO2 from electric power plants, issues CO2 allowances and establishes participation in regional CO2 allowance auctions.

Proponents tout RGGI as a successful program because participating states have “cut carbon pollution from their power plants by more than half, improved public health by cutting dangerous air pollutants like soot and smog, invested more than $3 billion into their energy economies, and created tens of thousands of new job-years”. Others have pointed out that RGGI was not the driving factor for the observed emission reductions. My latest evaluation of RGGI results found that the investments from RGGI auction proceeds were only directly responsible for 5.6% of the total observed annual reductions over the baseline to 2020 timeframe and that those investments reduced emissions at a rate of $818 per ton of CO2. I conclude that RGGI successfully raised money but has not provided cost-effective emission reductions or has had much to do with the observed CO2 emission reductions in the electric generating sector of the NE United States.

Third Program Review

One aspect of the program is a program review that is a “comprehensive, periodic review of their CO2 budget trading programs, to consider successes, impacts, and design elements”. On March 29, 2023 RGGI Inc. and the participating states gave an update on the status of the third program review. The presentation gave an overview of the program, explained how the review process works, described state activities, and described the electric sector analysis. Meeting materials are available:

The description of the program review update (video here) used the following slide. The process is initiated by the states defining revised goals and ambitions which kicks off technical modeling and analysis and a public stakeholder process. If you have questions about the process this is a good overview.

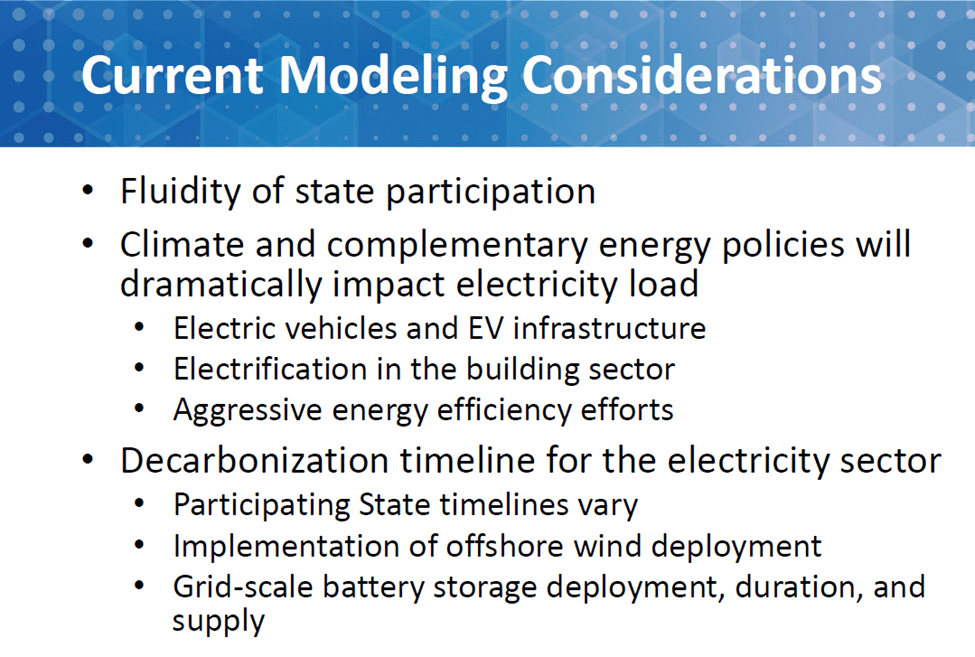

The meeting described the current modeling considerations, explained the approach and assumptions, and asked for comments on specific aspects of the modeling. My comments relate to the modeling analyses. David Coup from NYSERDA described the modeling analysis (video starting at 11:52) using the following slide. The presentation explained that the program review modeling is concerned with the regional cap trajectory, Cost Containment and Emissions Containment Reserves changes, and adjustments for banked allowances.

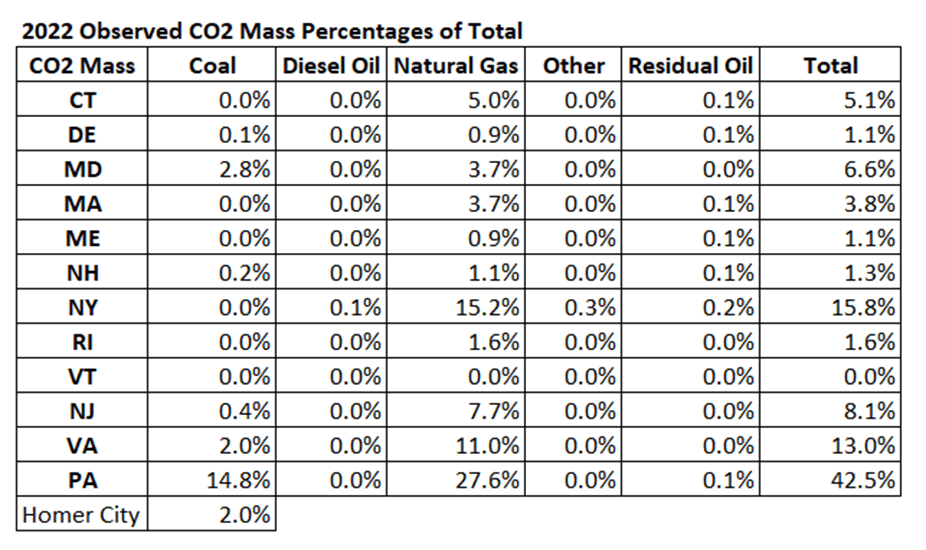

This round of modeling must contend with the “fluidity of state participation” which translates to what to do about Pennsylvania and Virginia. Pennsylvania participation is “still in effect” but it is still in litigation so there is a major uncertainty relative to the modeling. Virginia is going to cease participation at the end of 2023 and they have told RGGI that their participation should not be included in the modeling. The emissions from these two states are a significant portion of the current inventory so participation affects the potential for regional emission reductions. In 2022 Pennsylvania emissions were 42.5% of the total CO2 emissions of all RGGI states and Virginia was another 13% as shown below. From the standpoint of potential emission reductions note that Pennsylvania still had a significant amount of coal in 2022 and also note that the recently announced retirement of Homer City will result in a 2% reduction of overall RGGI emissions.

There are two other factors that complicate this modeling effort. The presentation noted that “climate and complementary energy policies will dramatically impact electricity load”. In other words, the primary decarbonization strategy for buildings and transport is electrification which will necessarily increase load. In addition, the decarbonization timeline for the electricity sector in states vary. Those timelines are primarily based on aspirational goals rather than a feasibility analysis to determine how fast wind and solar resources must be deployed to displace existing electric generation to make the mandated emission reductions. The presentation recognized that the implementation of offshore wind deployment and grid-scale battery storage deployment, duration, and supply as factors that add challenges and uncertainty to modeling the decarbonization transition.

In order to address these issues, they are looking at different ways of dealing with the uncertainty by developing “assumption sets based on load forecasts and availability of low-emitting generation” and various allowance supply scenarios. They think that adding cases will cover the range of outcomes given current electricity-sector developments and that the “results will inform development of potential policy cases”. While I appreciate the thought, I am concerned that political pressures will preclude any cases that don’t fit the narrative that political timelines will mandate development as needed to meet the schedules.

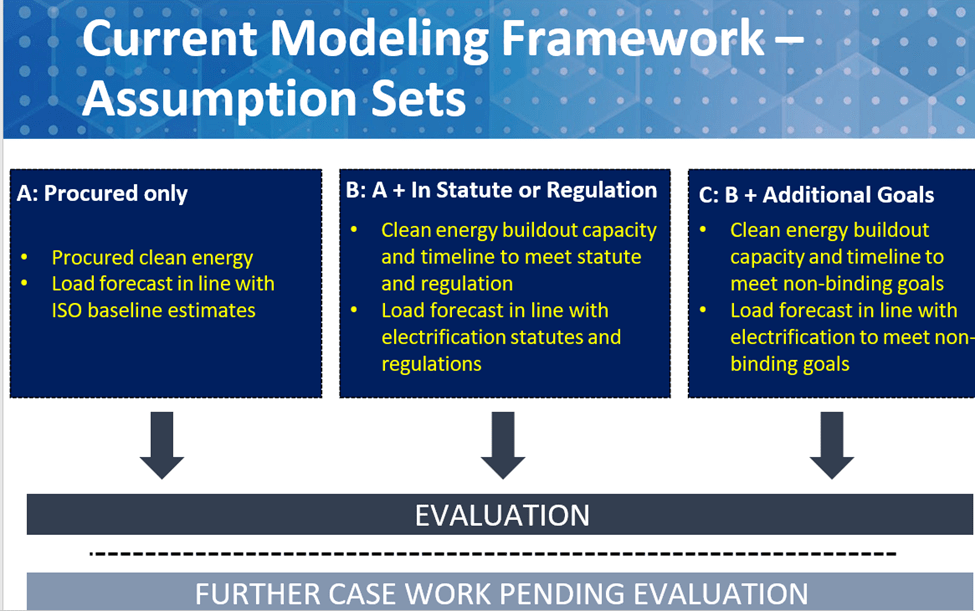

The load forecast and availability of low-emitting generation discussion (video at 21:20) provides the modeling framework. As shown in the slide below they are considering three assumption sets ranging from “procured” clean energy and energy forecasts in line with Independent System Operator baseline estimates to two levels of additional clean energy and load growth. Their definition of procured is that the project is “under contract”. This is a good example of my concern about the schedule because projects under contract may still be abandoned due to several reasons. My main concern is that the timelines have major implications. An increasingly large percentage of future EGU emissions reductions is only possible if clean energy deployment displaces fossil generating facilities because there are no other options left. There are significant uncertainties associated with clean energy development because of supply chain issues and the need for extensive supporting infrastructure.

Four specific questions for input from stakeholders were posed (video at 30:19)

- How comfortable are you with the assumptions that have been included?

- Are there other assumptions that need to be included in these scenarios?

- Is there anything that we can do to improve the understanding of the differences between the cases?

- For which scenarios are stakeholders most interested in seeing results for further Program Review consideration?

My comments addressed two of these questions: How comfortable are you with the assumptions that have been included and are there other assumptions that need to be included in these scenarios?

Fifth Compliance Period Status

One of my concerns about the assumptions included is that there are other uncertainties not included. In my initial comments on the Third Program Review my overall recommendation was to make no changes and see how the RGGI allowance market plays out the transition to the unprecedented emissions trading situation in which the majority of the RGGI allowances are held by entities who purchased allowances for investment rather than compliance purposes.

My comments described in detail my latest analysis of allowance holdings and emissions confirms compliance entities will have to obtain allowances from non-compliance entities to meet compliance obligations at the end of 2023. At the end of the fourth quarter of 2022 the RGGI Market Monitoring Report Q4 2022 noted that there were 231 million allowances in circulation. The report noted that approximately 148 million of the allowances in circulation (64 percent) are believed to be held for compliance purposes. I estimate that there were 176.6 million allowances in circulation at end of March 2023 and that approximately 89.8 million allowances (51%) were held for compliance purposes. I estimated the allowance status at end of the 2021-2023 compliance period as 224.9 million allowances in circulation before allowances are surrendered for 2023 emissions with 105.8 million allowances held for compliance purposes. Assuming that 2023 emissions would be equal to 2022 emissions for all the RGGI states including Pennsylvania means total emissions will be 193.3 million tons. That means 87.5 million allowances must be obtained from non-compliance entities for compliance and that the next compliance period will start with an allowance bank of only 31.6 million.

Those two unprecedented concerns are not included in the modeling assumptions. In the fifth compliance period ending December 31, 2023 the compliance entities are going to have to use allowances now held by non-compliance entities and in the sixth compliance period the allowance cap is going to be binding. I define a binding cap as one chosen arbitrarily without any feasibility evaluation. The environmental community has demanded a binding RGGI cap for years and it looks like they are going to get their wish in the 2024-2026 compliance period. My comments stated that these issues should included in the “are there other assumptions that need to be included in these scenarios?” question posed at the March 29 meeting. Given the importance of these uncertainties I expanded on my concerns.

Non-Compliance Entities

Based on the evaluation described above I estimate that compliance entities will be required to obtain allowances for compliance from non-compliance entities. In my opinion, it is reasonable to expect that the non-compliance entities that own allowances for investment purposes will expect a premium for their allowances because they know that the penalties for an out of compliance affected source are severe. This is unprecedented and no one knows what will happen so it is reasonable to see what happens before there are any decisions regarding changes to the allowance allocation trajectories.

There is another non-compliance entity issue. In previous comments I pointed out that at least one non-governmental environmental entity has purchased allowances and “will be retiring these allowances so that no power plant can use them to emit greenhouse gas”. I suggested that this ownership entity should be included as a new category in the Potomac Economics market monitoring reports and that a surrender account be established for individuals and organizations that want to use RGGI allowances for offsetting purposes. The recommendation was ignored so we are left to hope that the Potomac Economics market monitoring report non-compliance entity category has at least 87.5 million allowances that will be available for compliance purposes.

Observed Emission Reductions to Date

There is another uncertainty associated with future emission reductions. In my previous comments, I showed that fuel switching from coal and residual oil to natura gas has been the primary CO2 reduction methodology to date. Of particular importance to the future program is that the potential for future fuel switching is limited outside of Pennsylvania. The following table lists CO2 emissions for each state by primary fuel type. The retirement of the coal-fired Homer City facility was recently announced and that facility was responsible for 2% of 2022 emissions. If Pennsylvania joins RGGI as a full-fledged member and coal retirements from its facilities occur in the future the current reduction trajectory is feasible. If those conditions do not occur then the only way to produce reductions is by displacement with zero-emissions generating sources. Eventually, investments in zero-emissions resources will be the only method for reducing affected source emissions.

One of my problems with the RGGI cap and invest program is that while it is supposed to be a pollution control program in which the auction proceeds are invested in emission reduction strategies, the proceeds have not prioritized emission reductions. In my previous comments I noted that the total of the annual reductions claimed by RGGI in their annual Investments of Proceeds updates since 2009 is 2,818,775 tons while the difference in annual emissions between the baseline of 2006 to 2008 compared to 2019 emissions is 72,908,206 tons. Therefore, the RGGI investments are only directly responsible for less than 5% of the total observed reductions since RGGI began in 2009. (Note that I did an update for information through 2020 that did not change these findings.)

Binding Cap

Another uncertainty not included in the issues raised at the March 29 meeting is the binding cap. I define a binding cap as one chosen arbitrarily to meet some emission reduction target without considering the feasibility of emission reductions necessary to meet that target. The problem that advocates apparently do not understand is that CO2 control is different than other pollutants because there are no cost-effective controls available for existing facilities. Instead, CO2 reductions at electric generating facilities require development of zero-emissions resources to displace the need for electric energy output at affected sources. If the energy from those zero-emissions resources is insufficient to replace affected source generation, then the only compliance alternative left is to stop running. Unplanned outages due to a lack of allowances could lead to reliability issues.

The binding cap must be considered in the context of the reason for the observed emission reductions and the impact of inefficient RGGI proceeds for reductions. I recommended that assumptions addressing the binding cap issues need to be included in the RGGI scenarios. The RGGI states all have various CO2 emission reduction mandates that rely on electrification of other sectors. This will necessarily increase load at the same time the deployment of low-emitting generation will be the primary emission reduction methodology. EPA cap and trade programs such as the Cross State Air Pollution Rule established caps based on technological evaluation of control options. The RGGI reduction trajectory was established based more on arbitrary decarbonization timelines than a deployment schedule supported by a feasibility analysis. The modeling for this program review must include modeling analyses that consider the zero-emissions deployment schedules. Sensitivity analyses that consider delays to the deployment of wind and solar resources should also be included.

Conclusion

The March 29 meeting raised the important point that there are new uncertainties that need to be incorporated in the assumptions used for the modeling analyses associated with the third program review. My comments raised additional issues that add uncertainty and should be considered too.

RGGI asked “how comfortable are you with the assumptions that have been included.” Because future reductions will rely more heavily upon displacement of affected source energy production by wind and solar at the same time emission reductions in other sectors rely on increased electrification, I am particularly concerned about the load forecasts and availability of low-emitting generation assumptions. The impact of future load growth and the schedule for low-emitting generation deployment should be considered in the modeling at least by sensitivity analyses.

RGGI also asked if there are other assumptions that need to be included in these scenarios? The RGGI presentation noted significant uncertainties. I believe that two other uncertainties need to be considered. My analysis of the status of emissions and allowances shows that compliance entities will have to depend on allowances from the non-compliance entities for the fifth compliance period ending this year. That analysis also shows that when the sixth compliance period starts in 2024 there will be an extremely small allowance bank. I believe that these added uncertainties need to be addressed in the modeling for this program review.

The potential problems associated with a cap on allowances that forces affected sources to comply by not operating is an unrecognized issue. If an overly stringent cap results in an artificial energy shortage, then it will not reflect well on the RGGI states.