New York’s strange political process includes an annual legislative self-made crisis related to the budget which is just coming to a conclusion. This year the initial budget bills from the Governor, Senate and Assembly included significant policy aspects related to the Climate Leadership & Community Protection Act (Climate Act) that did not get included in the final budget bill but there are still some less impactful legislative proposals in the final draft I have seen. This post addresses the allocations for the proposed cap and invest program.

I have been following the Climate Act since it was first proposed. I submitted comments on the Climate Act implementation plan and have written over 300 articles about New York’s net-zero transition because I believe the ambitions for a zero-emissions economy embodied in the Climate Act outstrip available renewable technology such that the net-zero transition will do more harm than good. The opinions expressed in this post do not reflect the position of any of my previous employers or any other company I have been associated with, these comments are mine alone.

Climate Act Background

The Climate Leadership & Community Protection Act (Climate Act) established a New York “Net Zero” target (85% reduction and 15% offset of emissions) by 2050 and an interim 2030 target of a 40% reduction by 2030. The Climate Action Council is responsible for preparing the Scoping Plan that outlines how to “achieve the State’s bold clean energy and climate agenda.” In brief, that plan is to electrify everything possible and power the electric gride with zero-emissions generating resources by 2040. The Integration Analysis prepared by the New York State Energy Research and Development Authority (NYSERDA) and its consultants quantifies the impact of the electrification strategies. That material was used to write a Draft Scoping Plan. After a year-long review the Scoping Plan recommendations were finalized at the end of 2022. In 2023 the Scoping Plan recommendations are supposed to be implemented through regulation and legislation.

Cap and Invest Overview

As part of the Hochul Administration’s plan to implement the Climate Leadership & Community Protection Act (Climate Act), a market-based pollution control program called ‘’cap and invest” was proposed earlier this year in legislation associated with the budget. The Assembly budget bill does not include any cap and invest provisions other than mandates for the use of the revenues collected. This overview gives context for those provisions.

The Climate Act Scoping Plan identified the need for a “comprehensive policy that supports the achievement of the requirements and goals of the Climate Act, including ensuring that the Climate Act’s emission limits are met.” It claimed that the policy would “support clean technology market development and send a consistent market signal across all economic sectors that yields the necessary emission reductions as individuals and businesses make decisions that reduce their emissions” and provide an additional source of funding. The authors of the Scoping Plan based these statements on the success of similar programs but did not account for the differences between their proposal and previous programs. The Assembly budget bill Part TT proposal is similarly flawed.

The cap and invest proposal is a variation of a pollution control program called cap and trade. In theory, placing a limit on pollutant emissions that declines over time will incentivize companies to invest in clean alternatives that efficiently meet the targets. These programs establish a cap, or limit, on total emissions. For each ton in the cap an allowance is issued. The only difference between these two programs is how the allowances are allocated. The Hochul Administration proposes to auction the allowances and invest the proceeds but, in a cap-and-trade program, the allowances are allocated for free. The intent is to reduce the total allowed emissions over time consistent with the mandates of the Climate Act and raise money to invest in further reductions.

The Environmental Protection Agency administers cap and trade programs for sulfur dioxide (SO2) and nitrogen oxides (NOx) that have reduced electric sector emissions faster, deeper, and at costs less than originally predicted. In the EPA programs, affected sources that can make efficient reductions can sell excess allocated allowances to facilities that do not have effective options available such that total emissions meet the cap. Also note that EPA emission caps were based on the feasibility of expected reductions from addition of pollution control equipment and a schedule based on realistic construction times.

However, there are significant differences between those pollutants and greenhouse gas pollutants that affect the design of the proposed cap and invest program. The most important difference is that both SO2 and NOx can be controlled by adding pollution control equipment or fuel switching. Fuel switching to a lower emitting fuel is also an option for carbon dioxide (CO2) emissions but there are no cost-effective control equipment options. Consequentially, CO2 emissions are primarily reduced by substitution of alternative zero-emissions resources. For example, in the electric sector replacing fossil-fired units with wind and solar resources. The ultimate compliance approach if there are insufficient allowances available is to limit operations.

New York State is already in a cap and invest program with an auction for CO2 emissions from the electric generating sector. Although significant revenues have been raised, emission reductions due to the program have been small. Since the Regional Greenhouse Gas Initiative started in 2009, emissions in nine participating states in the Northeast have gone down about 50 percent, but the primary reason was fuel switching from coal and residual oil to natural gas enabled by reduced cost of natural gas due to fracking. Emissions due to the investments from the auction proceeds have only been responsible for around 15 percent of the total observed reductions.

The Hochul Administration has not addressed the differences between existing market-based programs and the proposed cap and invest program. Although RGGI has provided revenues, the poor emission reduction performance has been ignored despite the need for more stringent reductions on a tighter schedule to meet the arbitrary Climate Act limits. The Hochul Administration has not done a feasibility analysis to determine how fast the wind and solar resources must be deployed to displace existing electric generation to make the mandated emission reductions. Worse yet, the Climate Act requires emission reductions across the entire economy and the primary strategy for other sectors is electrification, so electric load is likely to increase in the future.

In late March, the Hochul Administration proposed a modification to the Climate Act to change the emissions accounting methodology to reduce the expected costs of the cap and invest program. New York climate activists claimed that the change would eviscerate the Climate Act and convinced the Hochul Administration to delay discussion of this aspect of the cap and invest proposal. This cost issue will have to be resolved in the upcoming debate over the cap and invest program.

In addition, the Hochul Administration has proposed a rebate to consumers that will alleviate consumer costs and this is included in the final budget bill. This raises a couple of issues. The market-based control program intends to raise costs to influence energy choices, so if all the costs are offset there will not be any incentive to reduce consumer emissions by changing behavior. The other issue is that the auction proceeds are supposed to be invested to reduce emissions. If insufficient investments are made to renewable resources, then deployment of zero-emission resources to offset emissions from fossil generating units will not occur.

The final issue related to the cap and invest proposal is that it provides compliance certainty but you have to be careful what you wish for. The plan is to match the allowance cap with the Climate Act emission reduction mandates. As noted previously, there are limited options available to reduce CO2 emissions. The primary strategy will be developing zero-emissions resources that can displace emissions from existing sources. That implementation is subject to delays due to supply chain issues, permitting delays, and costs as well as other reasons that the state’s transition plan has ignored. Once all the other compliance alternatives are exhausted, the only remaining option is to reduce the availability of fossil fuel and its use. Worst case could mean no fuel for transportation, electricity generation or home heating if the allowances run out.

Part TT in Assembly Budget Bill

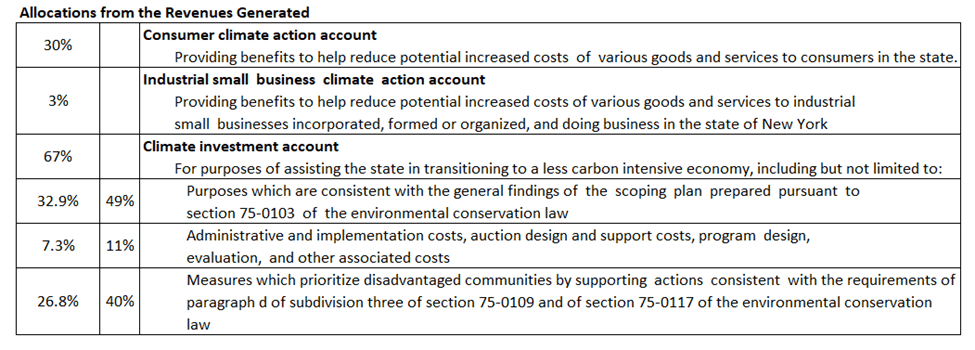

The primary purpose of this post is to address Part TT of the Assembly budget bill. The legislation proposes to amend Section 1854 of the Public Authorities Law by adding three new subdivisions 24, 25 and 26. I will only address the new § 99-qq. New York Climate Action Fund. Proceeds from the cap-and-invest auction are intended to go to the Climate Action Fund and the legislation mandates that the revenues must not be reallocated at the whim of the Administration. It requires the comptroller to setup the “following separate and distinct accounts”:

- Consumer Climate Action Account;

- Industrial Small Business Climate Action Account; and

- Climate Investment Account.

The accounts have mandated allocations and purposes. The Consumer Climate Action Account is allocated 30% of the revenues collected and the money “shall be expended for the purposes of providing benefits to help reduce potential increased costs of various goods and services to consumers in the state.” The Industrial Small Business Climate Action Account is allocated no more than 3% for “the purposes of providing benefits to help reduce potential increased costs of various goods and services to industrial small businesses incorporated, formed or organized, and doing business in the state of New York.” The Climate Investment Account is allocated the remaining 67% for the purposes of assisting the state in transitioning to a less carbon intensive economy.

The Climate Investment Account has three components. The first component covers “purposes which are consistent with the general findings of the scoping plan prepared pursuant to section 75-0103 of the environmental conservation law” I presume that means investments in recommended strategies to reduce GHG emissions. The second component covers “administrative and implementation costs, auction design and support costs, program design, evaluation, and other associated costs”. The third component includes “measures which prioritize disadvantaged communities by supporting actions consistent with the requirements of paragraph d of subdivision three of section 75-0109 and of section 75-0117 of the environmental conservation law, identified through community decision-making and stakeholder input, including early action to reduce greenhouse gas emissions in disadvantaged communities.” Section 75-0117 states:

State agencies, authorities and entities, in consultation with the environmental justice working group and the climate action council, shall, to the extent practicable, invest or direct available and relevant programmatic resources in a manner designed to achieve a goal for disadvantaged communities to receive forty percent of overall benefits of spending on clean energy and energy efficiency programs, projects or investments in the areas of housing, workforce development, pollution reduction, low income energy assistance, energy, transportation and economic development, provided however, that disadvantaged communities shall receive no less than thirty-five percent of the overall benefits of spending on clean energy and energy efficiency programs, projects or investments and provided further that this section shall not alter funds already contracted or committed as of the effective date of this section.

Funding Allocations

I am particularly concerned with the funding allocations. Ultimately the cap and invest program is supposed to invest funds received in the recommended strategies to achieve the net-zero transition. The Climate Action Council’s Scoping Plan presumes that investors will make fund all the infrastructure necessary to reduce GHG emissions consistent with the Climate Act targets. However, unless subsidies are available, I do not think there will be sufficient private investment to develop all the necessary infrastructure. This legislation does not recognize this challenge.

The following table breaks down the allocations. The Consumer Climate Action Account is a gimmick. The state proposes to quietly take money on one hand and then turn around and loudly give some of it back on the other hand. Who gets what and has anyone bothered to figure out if the giveback makes anyone whole for the costs? The Industrial Small Business Climate Action Account is intended to appease the companies that will inevitably end up paying more to be less competitive. The Climate Act is supposed to rectify climate and environmental justice inequities and the offered solution is a 40% investment in affected communities. In the following table I assumed that the 40% would come out of the climate investment account. New York is already in the Regional Greenhouse Gas Initiative (RGGI) cap and invest program. In Fiscal Year 22-23, the RGGI operating plan costs for program administration, state cost recovery and the pro rata costs to RGGI Inc for things like auction services and market monitoring comprised 10.9% of the total expenses. I assumed those costs only relate to the Climate Investment Account. That leaves 49.1% for this account. Those are the Climate Investment Account revenues that can be invested in the infrastructure necessary to subsidize the infrastructure requirements for the net-zero transition.

Discussion

I support the intent of the proposed legislation to prevent using the revenues raised in the cap and invest auction for purposes other than its intended use. In the past, RGGI revenues have been overtly transferred to balance the budget and, as far as I am concerned, RGGI revenues are still used to cover inappropriate costs. However, the proposed legislation still undermines the GHG emission reduction potential of the cap and invest program.

In the previous table I broke down the allocations in the Climate Investment Account relative to the total revenues generated. When you apportion the 67% allocation to the Climate Investment Account between the three categories it does not appear that the authors of the legislation have accounted for the challenge of implementing the infrastructure necessary to make the reductions necessary. The administrative component will account for 7.3% of the total revenues. The investments in the disadvantaged communities are necessary to protect those least able to afford the inevitable increased cost of energy. However, the results from the NY RGGI funding status report indicate that energy efficiency, energy conservation, and other indirect emission reduction strategies are not very cost effective so despite revenues of 26.8% of the total I do not expect significant reductions. Most importantly, only 32.9% of the auction revenues will be available to subsidize the emission reduction strategies necessary to displace the use of fossil fuels and reduce GHG emissions.

The Hochul Administration and authors of this legislation apparently do not recognize the RGGI investment results that show that emissions due to the investments from the auction proceeds have only been responsible for around 15 percent of the total observed reductions. This is a challenge that should be a priority for investment planning. The allocation of less than a third of the total revenues shows that they don’t get it.

In addition, the Consumer Client Action account is intended to provide a rebate that will alleviate consumer costs. However, the market-based control program intends to raise costs to influence energy choices, so if all the costs are offset there will not be any incentive to reduce consumer emissions by changing behavior.

My biggest concern is the lack of recognition that the auction proceeds must be invested to reduce emissions. If insufficient investments are made to renewable resources development, then deployment of zero-emission resources to offset emissions from fossil generating units will not occur. The Scoping Plan and Integration Analysis provide no details for the total expected costs so we don’t know how much money has to be raised. The Hochul Administration has not detailed what assets are supposed to fund those costs nor provided a timeline for developing resources needed to meet the Climate Act emission reduction mandates.

Conclusion

The cap and invest proposal is a well-meaning but dangerous plan. It will increase the cost of energy in the state. If the costs are set such that the investments will produce the necessary emission reductions to meet the Climate Act targets, it is likely that the costs will be politically toxic. If the investments do not effectively produce emission reductions, then the compliance certainty feature will necessarily result in artificial energy shortage. Given all the uncertainties it is probably best to not pass any implementing legislation until there is time to discuss policy implications.