I have regularly prepared updates on the Regional Greenhouse Gas Initiative (RGGI) annual Investments of Proceeds report. Last year I described the implications of the report relative to the finalized Third Program Review. This year the report comes out at a time when the costs have risen sharply and the trend of emission reductions has stalled while at the same time the future annual allowance reduction trajectory mandates an annual reduction of over 10% between 2026 and 2027 and beyond. In this post I review the 2024 investment proceeds to see if there is any indication that auction proceeds are being invested better.

Dealing with the RGGI regulatory and political landscapes is challenging enough and agency retribution is enough of a threat that affected entities seldom see value in speaking out about fundamental issues associated with the program. I have been involved in the RGGI program process since its inception and have no such restrictions when writing about the about problems with the RGGI program. I have worked on every cap-and-trade program affecting electric generating facilities in New York including RGGI, the Acid Rain Program, and several Nitrogen Oxide programs, since the inception of those programs. I also participated in RGGI Auction 41 successfully winning allowances and holding them for several years. The opinions expressed in this post do not reflect the position of any of my previous employers or any other organization I have been associated with, these comments are mine alone.

Background

RGGI is a market-based program to reduce greenhouse gas emissions (GHG) (Factsheet). It has been a cooperative effort among the states of Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New York, Rhode Island, and Vermont to cap and reduce CO2 emissions from the power sector since 2008. New Jersey was in at the beginning, dropped out for years, and re-joined in 2020. Virginia joined in 2021, withdrew in 2024, and rejoined effective July 1, 2026, and Pennsylvania considered joining but has since decided not to join. According to a RGGI website:

The RGGI states issue CO2 allowances that are distributed almost entirely through regional auctions, resulting in proceeds for reinvestment in strategic energy and consumer programs. Programs funded with RGGI investments have benefited local businesses, low-income communities, industrial facilities, and households throughout the region.

Proceeds were invested in programs including energy efficiency, clean and renewable energy, beneficial electrification, greenhouse gas abatement and climate change adaptation, and direct bill assistance. Energy efficiency continued to receive the largest share of investments.

Despite claims about the success of RGGI, the reality is that the only thing it is good at is raising money. Suggestions that RGGI has been responsible for the observed reductions in CO2 emissions over the life of the program ignore the importance of fuel switching and the poor performance of RGGI auction proceed investments in reducing emissions. I document these observations below.

Proceeds Investment Report

The 2024 investment proceeds report was released on June 26, 2026. According to the press release: “In 2024, $856 million in RGGI proceeds were invested in programs including energy efficiency, clean and renewable energy, beneficial electrification, greenhouse gas abatement, and direct bill assistance. Over their lifetime, these 2024 investments are projected to provide participating households and businesses with $2.6 billion in energy bill savings and avoid the emission of 4.4 million short tons of CO2..” The report breaks down the investments into major categories. The 2024 investment report explains:

Energy efficiency makes up 46% of 2024 RGGI investments and 54% of cumulative investments. Programs funded by these investments in 2024 are expected to return about $1.8 billion in lifetime energy bill savings to more than 127,000 participating households and 2,000 businesses in the region and avoid the release of 2.1 million short tons of CO2.

Clean and renewable energy makes up 6% of 2024 RGGI investments and 11% of cumulative investments. RGGI investments in these technologies in 2024 are expected to return over $421 million in lifetime energy bill savings and avoid the release of more than 1.1 million short tons of CO2.

Beneficial electrification makes up 16% of 2024 RGGI investments 6% of cumulative investments. RGGI investments in beneficial electrification in 2024 are expected to avoid the release of 1.2 million short tons of CO2 and return over $167 million in lifetime savings.

Greenhouse gas abatement and climate change adaptation makes up 4% of 2024 RGGI investments and 6% of cumulative investments. RGGI investments in greenhouse gas (GHG) abatement and climate change adaptation (CCA) in 2024 are expected to avoid the release of more than 3,400 short tons of CO2.

Direct bill assistance makes up 23% of 2024 RGGI investments and 16% of cumulative investments. Direct bill assistance programs funded through RGGI in 2024 have returned over $197 million in credits or assistance to consumers.

Unfortunately, this official story about the virtues of RGGI investments does not square with reality.

Emission Reductions

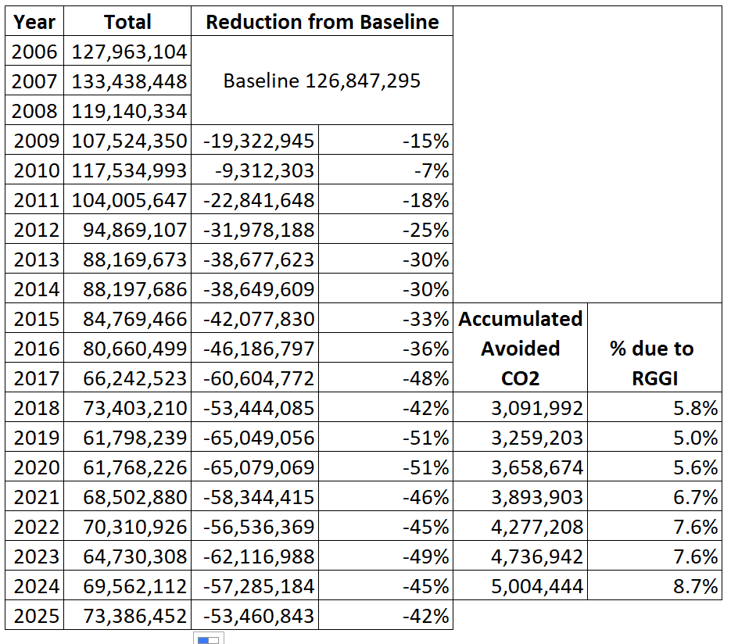

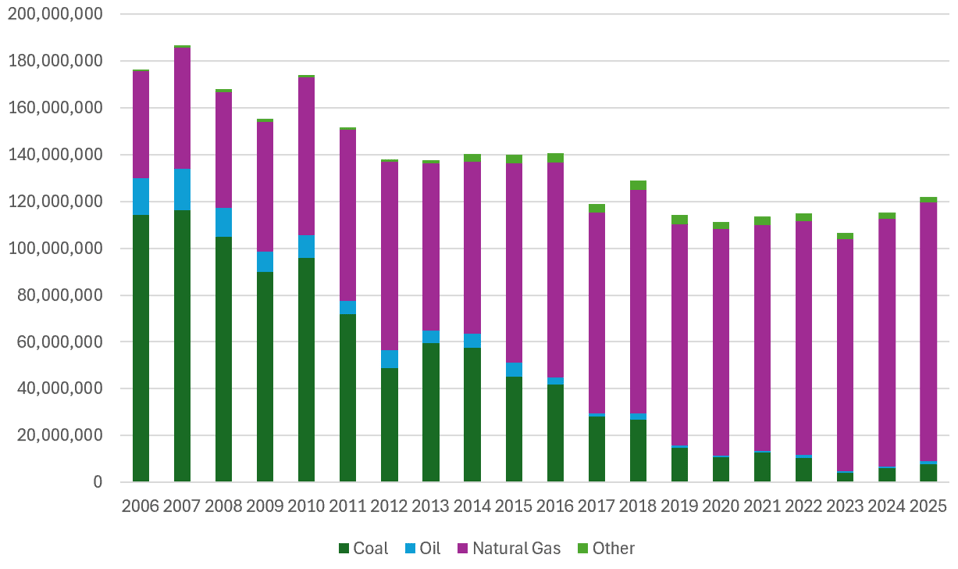

All my summaries of the RGGI Investment Proceeds reports have found the same results. Since the beginning of the RGGI program, RGGI funded control programs have been responsible for a small fraction of the observed reductions – only 8.7% in 2024 (Table 1). Figure 1 plots CO₂ emissions by fuel type across all eleven RGGI states from 2006 to 2025. What you see is fuel switching caused the reductions and that there are only minor opportunities for future fuel switching. Consequently, future reductions will have to rely on the deployment of zero-emission generating resources and load reductions which makes cost-effective emission investments important.

Table 1: State-Level CO2 Emissions for Nine RGGI States 2009 to 2024

Figure 1: Eleven State RGGI CO₂ Emissions (short tons) for all Programs 2006–2025

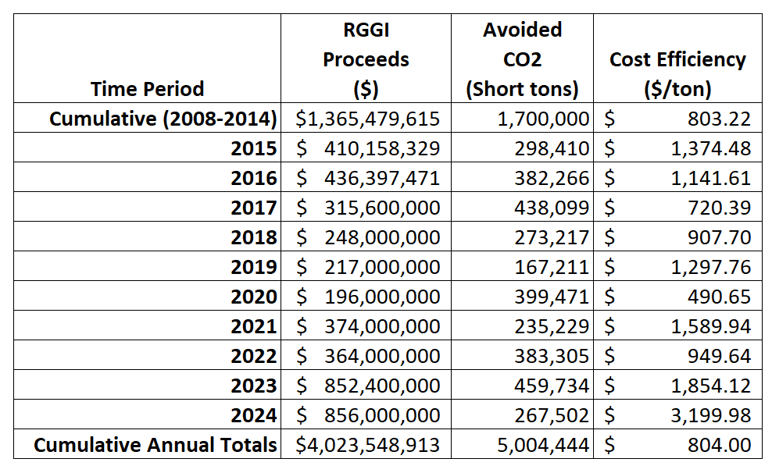

The importance of cost-effective investments for emission reductions is unacknowledged by the RGGI states. I calculate cost effectiveness by dividing the RGGI total investments divided by the estimated avoided CO2 emissions. In 2022 the CO2 emission reduction efficiency was $949 per ton of CO2 reduced, in 2023 the cost per ton reduced increased to $1,854, and in 2024 the cost per ton reduced reached $3200 per ton. It is not clear why there are such big changes. There is no obvious change in investment strategies, but the avoided annual CO2 emissions went down 42% in 2024 from 2023. I suspect that the calculation methodology contributes to these numbers but this cannot be confirmed because there is insufficient documentation. Nonetheless, if the RGGI states prioritized emission reduction efficiency then the trend should reverse.

Table 2: Accumulated Annual RGGI Proceeds, Avoided CO2, and Cost Efficiency

Emission Reduction Costs

RGGI is supposed to be an emissions reduction program. On July 3, 2025, RGGI announced the results of the Third Program Review that modified the requirements for future reductions. Based on my analysis of the planned revisions, the RGGI States only delayed the inevitable reckoning of the futility of this program to achieve the goal of a “zero-emissions” electric system. The RGGI summary of the revisions states that the revised mandated reductions will “decline by an average of 8,538,789 tons per year, which is approximately 10.5% of the 2025 budget” from 2027 to 2033.

The emission proceeds reports can be used to estimate expected costs if RGGI investments were the only source of emission reductions. Table 3 lists the cost per ton of CO2 removed of the RGGI investments from 2015 to 2024, the cost to reduce 8,538,789 tons per year using their observed costs, and the RGGI proceeds for each year. In 2024 the Third Program Review mandated annual emission reduction multiplied by the cost per ton ($1,854) totals $27.3 billion but the RGGI proceeds were only $0.86 billion. Even using the cost over the entire 10-year period of $1,126 per ton, it would cost $9.6 billion to make the reductions mandated. This is still far short of the proceeds available.

Table 3: Annual RGGI Cost Efficiency, Cost to Meet 2027 RGGI Annual Reduction, and Annual Proceeds

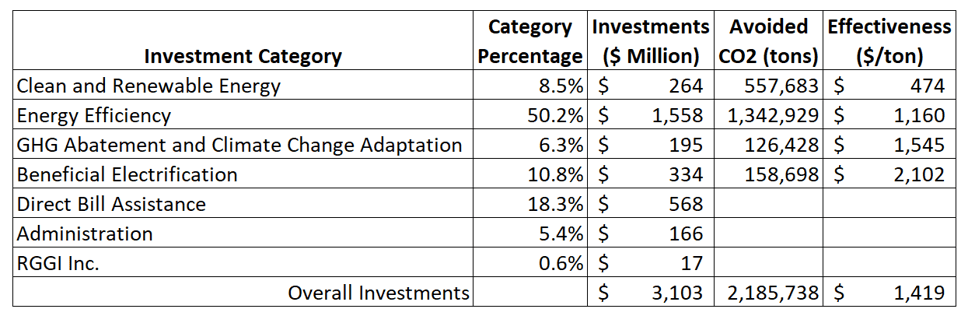

Investment of Proceeds Summary

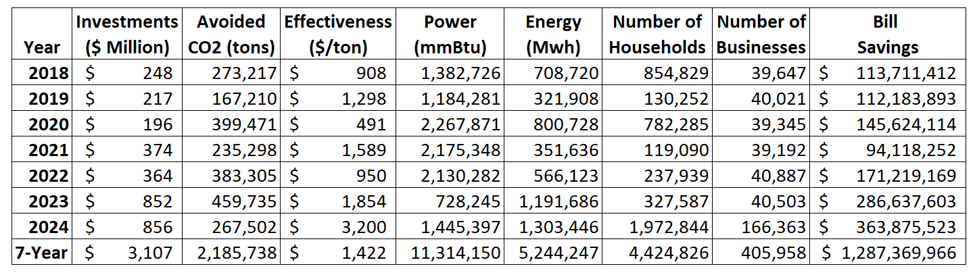

The 2024 investment proceeds report breaks down the investments into major categories. I added the annual values for each category to provide the following summary (Table 4). Note that the overall cost effectiveness is $1,422 per ton avoided. Clearly the proceed investment strategy is not emphasizing emission reduction effectiveness. It is encouraging that savings of $1.3 billion are claimed but total investments are $3.1 billion. In my opinion, these numbers are inconsistent with claims that RGGI is successful.

Table 4: RGGI Proceeds Report Investment Category Annual Totals

Cost Effectiveness Implications

One of my big concerns about any cost on carbon emissions is that it is a regressive stealth tax on energy. There is a tradeoff between trying to minimize those impacts and reducing emissions. In the last seven years $568 million or 18% of the RGGI auction proceeds went to direct bill assistance, which is good but that means that much less was available to reduce emissions (Table 5). Throw in the $166 million over the last seven years for administration that means that 24% of the RGGI auction proceeds were not used to reduce emissions.

Table 5: Summary of Recent RGGI Categorial Investments and Avoided Emissions Over the Last 7 Years

This article compares the cost effectiveness of emission reductions for the following investment categories: energy efficiency, clean and renewable energy, beneficial electrification, greenhouse gas abatement and climate change adaptation (Table 5). For the investment categories that provided emission reductions Clean and Renewable Energy was the most effective way to reduce emissions. As far as I can tell this category provides the most funding for projects that directly reduce emissions. It is encouraging that the energy efficiency is less than the average over all categories. This means that energy efficiency programs targeted at low- and middle-income households most affected by this energy tax will provide effective emission reductions but only at a cost near $1,160 per ton.

On the other hand, programs promoting the research and development of GHG abatement and climate change adaptation are less effective at reducing emissions. Perhaps a greater emphasis on programs promoting reduction of emissions in the power generation sector and advanced energy technologies and less emphasis on programs for the reduction of vehicle miles traveled, tree-planting projects designed to increase carbon sequestration, and climate adaptation and community preparedness initiatives would improve emission reduction efforts consistent with the emission reduction goal of RGGI.

The worst emission reduction programs are associated with beneficial electrification that are “designed to reduce fossil fuel consumption by implementing or facilitating fuel-switching to replace direct fossil fuel use with electric power“ for non-generating sources. This category was added recently. There are two ways to look at the high numbers. On one hand, it could be that it recognizes that reductions of overall fossil fuel consumption require efforts across all sectors. On the other hand, I think it inappropriately transfers costs to the electric sector that do not provide efficient emission reductions at a time when reductions are needed to achieve the accelerated allowance cap reductions.

My biggest concern is that RGGI funding priorities do not reflect the necessary funding required to meet the annual reduction mandates in the recently approved Third Program Review modifications. These results show that RGGI investments will not fund the emission reductions mandated. That leaves the question – where will the reductions come from?

Conclusion

The closing price of the early June RGGI allowance auction increased 40% since March. Claims that RGGI is a successful emission reduction program are inconsistent with the observations. The amount raised falls far short of the funds necessary to reduce RGGI emissions in accordance with Third Program Review requirements. Investment priorities are inconsistent with the emission reduction objectives. Finally, emission reductions associated with RGGI investments only account for 8.7% of the observed reductions. These results support my belief that RGGI now poses unacceptable affordability and reliability risks and needs immediate, fundamental revision.