The New York Power Authority (NYPA) recently published for public comment the draft first update to its inaugural Strategic Plan for “developing new renewable energy generation projects to supply New Yorkers with affordable, reliable, and emissions-free electricity.” Dennis Higgins graciously agreed to let me publicize his comments on the draft.

Dennis Higgins passes on his commentaries associated with New York’s Climate Leadership and Community Protection Act (Climate Act) to me. He taught for just a few years at St Lawrence and Scranton University, but spent most of his career at SUNY Oneonta, teaching Mathematics and Computer Science. He retired early, several years ago, in order to devote more time to home-schooling his four daughters. Dennis and his wife run a farm with large vegetable gardens where they keep horses and raise chickens, goats, and beef. He has been involved in environmental and energy issues for a decade or more. Although he did work extensively with the ‘Big Greens’ in efforts to stop gas infrastructure, his views on what needs to happen, and his opinions of Big Green advocacy, have forced him to part ways with their renewable energy agenda.

NYPA Strategic Plan

The New York political process and its one party rule uses the threat of shutting down state agencies to hijack annual budget vote to also include major policy legislation like the Climate Act. Recently it seems that every budget bill includes another New York energy policy mandate. The NYPA renewables responsibilities is an example:

The 2023-24 Enacted State Budget significantly expanded the New York Power Authority’s role in the renewable energy sector. Specifically, the new authority allows NYPA to plan, design, develop, finance, construct, own, operate, maintain and improve renewable energy generation projects to maintain an adequate and reliable supply of electric power and energy and support New York State’s renewable energy goals established in the Climate Leadership and Community Protection Act.

I think that mixing energy policy and politics is a recipe for disaster. The hubris of the supporters of energy policy knows no bounds. It is not only that their legislation mandates the impossible, but they also hamstring organizations in the state responsible for providing affordable, clean, and reliable electricity. Upset that the deployment of renewable energy was not progressing fast enough to save the planet, the legislation forced NYPA to develop a strategic plan to deploy more renewable energy.

NYPA published a draft of its Updated Strategic Plan on July 29, 2025, which details NYPA’s efforts to develop, own and operate renewable generation and energy storage projects to improve the reliability and resiliency of New York’s grid. The draft Updated Strategic Plan includes 20 new renewable generation projects and four energy storage projects. The plan also includes three new project portfolios that contain 152 storage systems. The new projects are located in every region throughout the state and represent a combined capacity of more than 3.8 gigawatts (GW). Including the first tranche of projects identified in the inaugural strategic plan—approved by the NYPA Board of Trustees in January—NYPA’s draft Updated Strategic Plan includes 64 projects and portfolios representing nearly seven gigawatts of capacity—enough electricity to power nearly seven million homes.

Cult Comments

Submitted comments on the 2025 NYPA Renewables Draft Updated Strategic Plan can be viewed. To give you a flavor of the political constituency that advocated for NYPA to have a role in renewables development I extracted the most common scripted comment. Gary Abernathy perfectly describes the people who submitted the scripted comments as “Worshipers at the altar of climate calamity”.

The worshipers have no concept of energy reality. There are multiple reasons that deployment is slower than envisioned by the authors of the Climate Act. They demand that NYPA double down on the number of public renewables going from the proposed 7 GW to 15 GW by 2030 because we need to “comply with the Climate Act, lower electricity bills, create 25,000 green union jobs, and end our fossil fuel dependence.” The reason is “we face life-threatening heat waves, flash floods, skyrocketing energy bills, and an attack on climate action from the federal government.” All emotion and no substantive justification. In the real world wishing hard will not overcome the supply chain issues, permitting concerns, financing problems with higher interest rates, and skilled tradesmen shortages problems that have delayed deployment.

Higgins Comments

Higgins prepared extensive comments that questioned whether any energy plan “reliant upon low-capacity factor, land hungry assets will prove reliable or affordable.” He also raises an important consideration for Upstate New Yorkers: will requiring the upstate region to forfeit land in what will prove a failed effort to power metro New York pass the ‘environmental justice’ litmus test.

His comments cover six points:

- NERC on the NY plan

- Neither academic nor empirical evidence indicate the state plan will succeed

- NERC warning — IBRs undermine grid reliability

- Capacity markets hammered by intermittent resources increasing energy costs and undermining reliability

- Intermittent resources will not prove economical or reliable according to Sweden and others

- NYISO has repeatedly warned of reliability issues

The first point addresses interconnection issues with neighboring jurisdictions. He notes that the New York plan “assumes markets will be available for our excess wind and solar energy” so that we can sell excess when it is not needed. He also points out that we will also be dependent upon our neighbors when New York wind and solar resources are not enough to support our needs. Higgins explains that the North American Energy Reliability Corporation (NERC) has highlighted risks to the bulk power system from wind and solar deployments that require the massive transmission upgrades needed for those energy transfers.

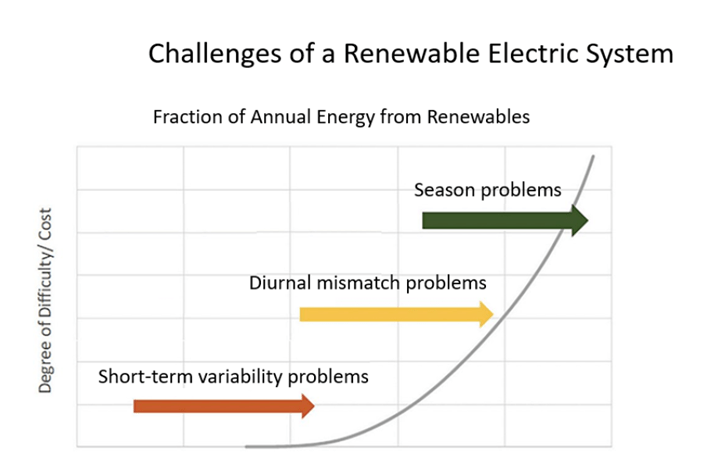

Higgins second point is one I constantly reiterate. Academic studies and empirical evidence do not support New York’s renewable push. He references the following National Renewable Energy Laboratory (NREL) chart that he says “shows the asymptotic costs of a system as penetration of renewables increases. Expensive battery energy storage can somewhat solve the “short term” variability of intermittent resource generation. But there is no day-night or seasonal solution.” I would add that the chart should also include the long duration dark doldrum event problem in the upper right portion of the curve. New York organizations responsible for the electric system all agree that a new dispatchable emission-free resource (DEFR) is needed. I believe that including it would extend the graph exponentially higher.

In his third argument Higgins points out that NERC has also warned that inverter-based resources undermine grid reliability. He quotes a NERC report:

Since 2016, NERC has analyzed numerous major events totaling more than 15,000 MW of unexpected generation reduction. These major events were not predicted through current planning processes. Furthermore, NERC studies were not able to replicate the system and resource behavior that occurred during the events, indicating systemic deficiencies in industry’s ability to accurately represent the performance of IBRs and study the effects of IBR on the bulk power system (BPS).

The fourth problem is that capacity markets are hammered by intermittent resources that increase energy costs and undermine reliability. The necessity to have firm dispatchable resources needed to back up intermittent wind and solar means that in jurisdictions that are further down the renewable deployment path there is an increased need for peaker power plants that burn natural gas. He describes the perverse economics that result. This will exacerbate New York’s energy affordability crisis

Higgins makes another point that I often raise. Evidence from other jurisdictions shows that intermittent resources will not prove economical or reliable. He cites results that show that

Controlling for country fixed effects and the rich dynamics of renewable energy capacity, we show that, all other things equal, a 1% percent increase in the share of fast reacting fossil technologies is associated with a 0.88% percent increase in renewable generation capacity in the long term.

Translated that means that for every MW of installed renewable capacity fast reacting dispatchable resources are necessary. The only available resource is fossil-fired generators. New York’s fossil fleet is aging. Consequently, we are going to have to replace all the fossil plants in the long term or rely on more expensive battery storage and DEFR. How can anyone claim that wind and solar are cheaper when they need one for one capacity backup is a mystery to me.

The final point that Higgins makes is that the New York Independent System Operator (NYISO has repeatedly warned of reliability issues. He quotes the latest Power Trends report:

As traditional fossil-fueled generation deactivates in response to decarbonization goals and tighter emissions regulations, reliability margins on the grid are eroding. Further, the remaining fossil-fueled generation fleet, which provides many of the essential reliability services to the grid, is increasingly made up of aging resources, raising further concerns about grid reliability. Strong reliability margins enable the grid to meet peak demand, respond to sudden disturbances, and avoid outages. They also support the grid’s ability to respond to risks associated with extreme weather conditions. As these margins narrow, consumers face greater risk of outages if the resources needed for reliability are unavailable due to policy mandates or failures associated with aging equipment.

Higgins raises substantive issues that could derail the net-zero transition. The political mandate to force NYPA to build as much renewable capacity as possible as quickly as possible ignores the very real possibility that the unresolved need for DEFR may mean that the renewable approach is a false solution. Obviously, New York needs to pause implementation and consider the schedule and ambition of the Climate Act.

Request

Please consider submitting comments for the proceeding. Written comments on the NYPA Renewables Strategic Plan can be submitted through Sept 12th here: https://publiccomments.nypa.gov/. Explain that you are worried about costs and reliability and suggest that the strategic plan should take those factors into account.

State agencies tend to count the number of comments that support their positions to justify going ahead with their plans. Even if you submit a comment that only says you agree with Vincent Gambini’s response to the scripted comments that say NYPA should build 15 GW of renewables by 2030, it would be useful. For once, I would like to see comments from those of us outside the cult of climate catastrophes outnumber those zealots.

Conclusion

This process is yet another component of the Climate Act net-zero transition. Even thought the costs are beginning to impact New York utility bills. the impacts of the Climate Act still are flying under the radar of most people. It is just getting started and it would be better to stop it now than wait. Contact your elected officials and demand accountability.