The Acadia Center recently published a post titled “Virginia is for Lovers, and RGGI is for Lower Energy Costs,” arguing that Virginia’s reentry into the Regional Greenhouse Gas Initiative (RGGI) will make energy more affordable. That narrative is increasingly at odds with both recent auction results and the actual mechanics of how RGGI costs flow through wholesale power markets and retail bills. This post explains why the Acadia Center story is incomplete at best and dangerously misleading at worst.

Dealing with the RGGI regulatory and political landscapes is challenging enough and agency retribution is enough of a threat that affected entities seldom see value in speaking out about fundamental issues associated with the program. I have been involved in the RGGI program process since its inception and have no such restrictions when writing about the about problems with the RGGI program. I have worked on every cap-and-trade program affecting electric generating facilities in New York including RGGI, the Acid Rain Program, and several Nitrogen Oxide programs, since the inception of those programs. I also participated in RGGI Auction 41 successfully winning allowances and holding them for several years. The opinions expressed in this post do not reflect the position of any of my previous employers or any other organization I have been associated with, these comments are mine alone.

Acadia Center’s RGGI advocacy rests on a familiar trilogy of claims: emissions have fallen faster in RGGI states, retail electricity prices are lower than in non‑RGGI states, and reinvestment of auction proceeds delivers bill savings that outweigh allowance costs.

In its RGGI materials, Acadia Center touts that:

- CO₂ emissions from covered power plants are down nearly 50 percent in RGGI states since 2008.

- Economic growth and per‑capita GDP have been stronger in RGGI states than elsewhere.

- Retail electricity prices in RGGI states fell by about 3 percent while prices rose nearly 8 percent in other states over roughly the same period.

- Over 8 million households and 400,000 businesses have benefited from RGGI proceeds, with claimed future bill savings of more than 20 billion dollars.

Acadia then projects this regional story onto Virginia, arguing that carbon pricing revenues can fund energy efficiency and bill assistance programs that will leave households better off.

What these talking points omit are: what actually drove the emissions reductions, how small the RGGI “signal” is relative to other factors, and how the RGGI cost adder interacts with today’s tight supply‑demand balance and rising load from data centers and electrification.

Emissions Fell Mostly Because of Fuel Switching

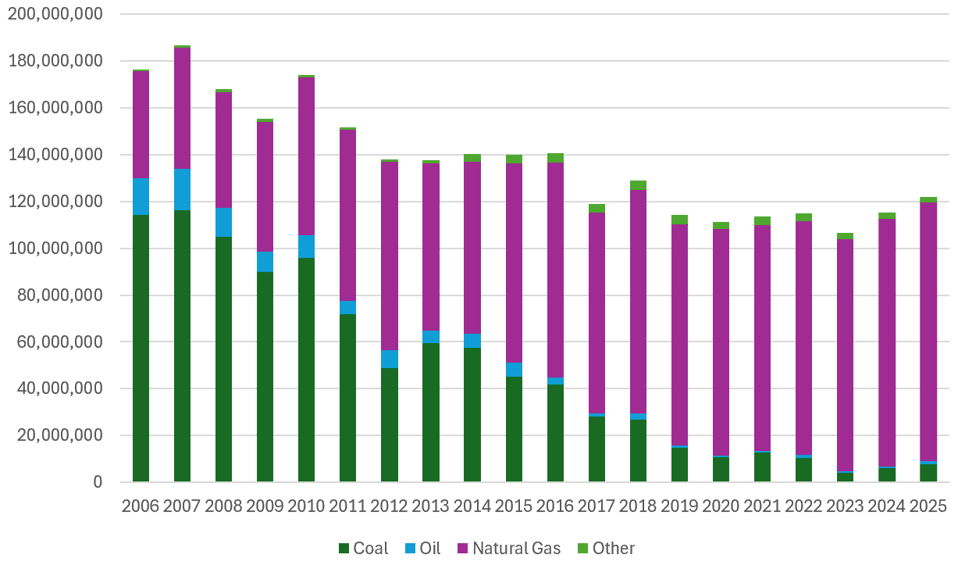

Acadia’s headline claim is that RGGI caused power‑sector CO₂ emissions to fall roughly 40 to 50 percent in the region. Figure 1 plots CO₂ emissions from all programs and all fuels in the eleven RGGI states from 2006 to 2025. The pattern is clear: emissions dropped primarily because of fuel switching from coal and oil to natural gas, not because of the modest CO₂ price RGGI imposed for most of its history.

Figure 1: Eleven State RGGI CO₂ Emissions (short tons) for all Programs 2006–2025

When I analyzed the 2023 RGGI investment proceeds report, I estimated that only about 7.6 percent of observed emission reductions could be attributed to RGGI‑funded projects, despite more than 7 billion dollars in auction proceeds since 2021. In other words, more than 90 percent of the emission reductions RGGI proponents celebrate came from factors that would have occurred with or without a RGGI cap‑and‑trade overlay.

If the emissions reductions were largely driven by cheap gas and non‑RGGI policy mandates, then it is intellectually dishonest to claim RGGI “delivered” those reductions and associated economic benefits. That matters for the future of RGGI, because the low‑hanging fruit from fuel switching has already been picked; repeating history is not an option.

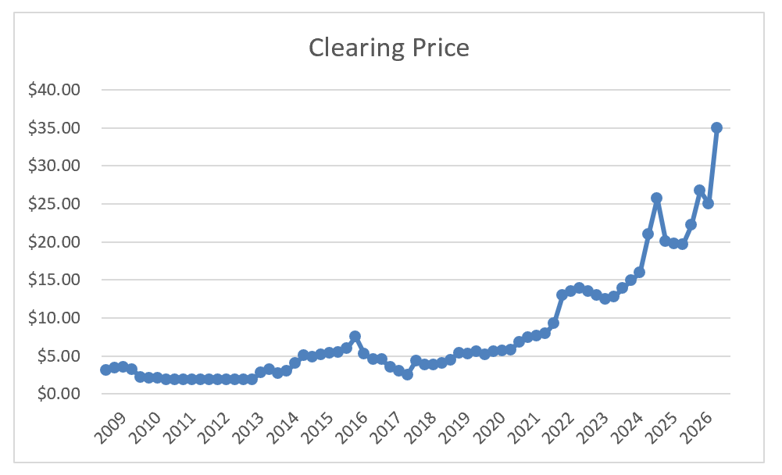

Acadia Center describes RGGI costs as a “very, very small percentage” of overall bills. That might have been a defensible talking point when allowance prices were in the single digits or low teens. It is no longer tenable at current levels.

The June 3, 2026 RGGI auction cleared at 35 dollars per ton, a 40 percent jump from the March 11, 2026 auction price of 24.99 dollars (Figure 2). RGGI itself acknowledged the affordability problem in its Auction 72 announcement, stating that the states intend to begin a scoping process to “continue to achieve reliable, clean electricity supply at affordable prices.”

Figure 2: RGGI Quarterly Auction Clearing Price

In 2025, RGGI‑affected sources emitted 86.4 million tons of CO₂, and the average auction price was 22.09 dollars per ton. That translates to 1.94 billion dollars in direct allowance costs to cover auction purchases. At a 35‑dollar allowance price, holding emissions constant, the direct cost rises by about 1.32 billion dollars to roughly 3.02 billion dollars per year.

These are not trivial numbers; they are large, recurring cost streams that must be recovered from someone. In practice, that “someone” is ratepayers across the region, including Virginia households and businesses once the state reenters.

The Hidden RGGI Cost Adder in Wholesale Markets

Acadia’s narrative focuses on what states do with auction revenue but ignores the way RGGI costs propagate through wholesale electricity markets. This omission is critical, particularly for a state like Virginia embedded in PJM with a large data‑center‑driven load growth problem.

When generators bid into daily wholesale markets, they embed the cost of RGGI allowances into their marginal energy bids. If the clearing price is set by a RGGI‑affected unit, then the clearing price includes the CO₂ allowance cost adder. Every unit dispatched at that price – including generators that do not have RGGI compliance obligations – gets paid the RGGI‑inflated clearing price.

The result is a two‑part cost impact:

- Direct compliance cost: RGGI‑covered generators pay for allowances, which they recover through higher energy prices.

- Indirect windfall cost: Non‑RGGI‑covered units receive higher revenues than they would have absent RGGI, because clearing prices are higher, even though they have no compliance costs.

In New York, I estimated that this market cost adder alone – the difference between what consumers pay in wholesale markets and the actual compliance costs – runs on the order of 1 to 3 billion dollars per year. Scaling that effect across all RGGI states suggests a regional market impact between roughly 2.7 and 8.1 billion dollars annually, depending on assumptions about generation and price formation.

Acadia Center’s claim that RGGI is an “energy affordability tool” glosses over this wholesale market dynamic, treating auction revenue as free money rather than as a tax on every megawatt‑hour consumers buy. For Virginia, plugging into this system at current prices means willingly imposing an added 10 to 20 dollars per megawatt‑hour on wholesale prices, according to industry estimates, just as bills are already under pressure from new infrastructure and load growth.

RGGI’s Cap Trajectory Is Detached from Reality

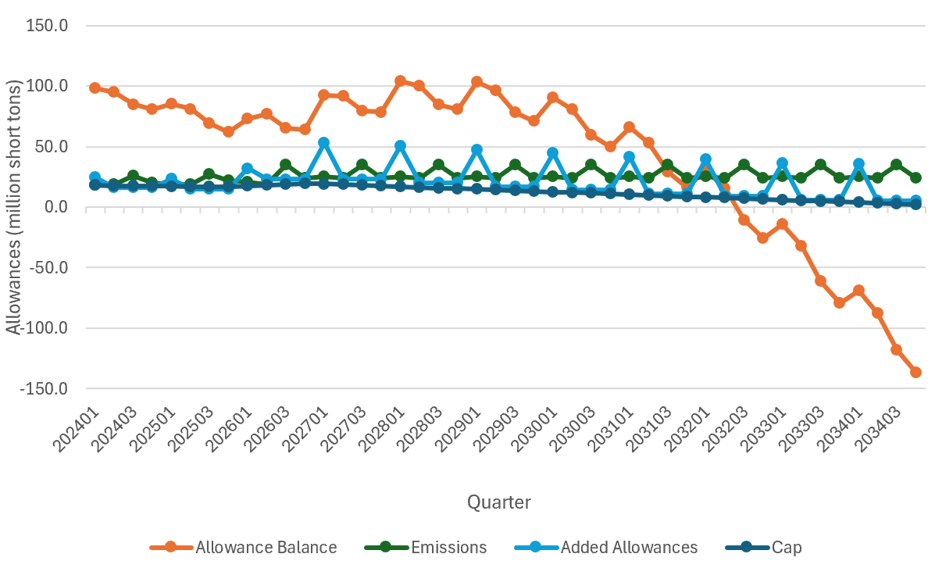

Acadia’s storyline assumes that RGGI’s cap trajectory is a reasonable reflection of technical and economic reality. The updated cap path adopted in mid‑2025 tells a different story.

I have found that the new cap reduction schedule cuts allowances by more than 10 percent of the 2025 budget each year from 2027 through 2033. The region has never sustained reductions of that magnitude, and recent years have seen emissions rise due to load growth and delays in clean generation deployment.

Once banked allowances are accounted for, my modeling indicates that the system could effectively “run out” of allowances as early as the second quarter of 2032. At that point, compliant units would face a choice between shutting down or operating out of compliance, neither of which is compatible with a reliable, affordable electric system (Figure 3).

Figure 3: Quarterly RGGI Allowance Balance, Emissions and Allowance Cap

RGGI’s own Auction 72 announcement admits that cost containment measures have already been exhausted in 2026: the primary cost control mechanism, the Cost Containment Reserve, was fully released in Auction 71, and no additional CCR allowances were available in Auction 72. When Virginia rejoins RGGI there will be another tranche of CCR allowances that I am sure will be released in the next auction. The market is signaling that the current cap path is too tight relative to realistic deployment trajectories for replacement generation.

Acadia Center ignores this looming supply‑demand imbalance in allowances, treating RGGI as a steady‑state policy rather than a program on track to collide with physical and economic constraints in the next decade.

Who Really Benefits from RGGI Revenue?

Acadia emphasizes that RGGI has generated over 9 billion dollars in proceeds, which states have invested in energy efficiency, clean energy, and bill assistance, benefiting millions of households and hundreds of thousands of businesses. That is technically true; those dollars do fund programs. The question is whether the emission reductions and bill savings they buy justify the costs – and whether the distributional impacts are as progressive as advertised.

My review of the 2023 RGGI investment report concluded that auction proceeds are being deployed inefficiently, with implied cost per ton reduced far above commonly cited social cost of carbon values. RGGI‑funded projects explain only a small fraction of observed emission reductions, while consuming billions of dollars in ratepayer‑funded resources.

Acadia’s “energy affordability” framing implies that these investments more than pay for themselves on consumer bills. Yet RGGI’s own announcement projects 20 billion dollars in future bill savings from investments, compared to allowance costs that, at current prices, could approach 30 billion dollars over a similar horizon if emissions remain near recent levels. Even if those bill savings materialize – a big if – they are not a free lunch; they are funded by the very bill surcharges the program imposes.

Moreover, the wholesale market cost adder described above means that a significant share of the burden falls on customers in the form of higher prices for every kilowatt‑hour, while benefits are concentrated in a subset of households and businesses that receive targeted efficiency or bill assistance. That might be a defensible redistribution if it were transparently acknowledged but calling the program an “affordability tool” obscures who pays and who gets paid.

RGGI states have long acknowledged leakage as a theoretical concern, but treated it as manageable. With Virginia’s reentry at current prices, leakage is no longer theoretical; it is inevitable, especially given the interconnected nature of PJM and the ability of non‑RGGI generators to serve load in RGGI states.[10][2][1]

Market Structure and Allowance Holdings Matter

Another blind spot in Acadia’s framing is how RGGI’s allowance market is structured and who holds allowances. Unlike some federal programs, RGGI does not publicly disclose ownership of allowances in detail; instead, its independent market monitor, Potomac Economics, reports aggregate holdings by broad categories such as “compliance‑oriented entities,” “investors with compliance obligations,” and “investors without compliance obligations.”

After Auction 72, compliance entities held 65 percent of allowances in circulation, and Potomac Economics estimates that 78 percent of allowances are held for compliance purposes. That leaves roughly 22 percent in the hands of entities that may be primarily motivated by investment returns rather than compliance.

There is also a fourth, largely unacknowledged category: non‑compliance entities that buy allowances explicitly to retire them, such as environmental organizations selling “carbon reduction certificates” to donors. While their holdings may be small today, the existence of such players underscores that not all allowances in circulation are actually available for resale or compliance.

In a tight market with a steeply declining cap, the presence of investors and voluntary retirement entities can exacerbate scarcity and volatility, driving up prices further. Acadia’s depiction of RGGI as a stable, well‑functioning market glosses over these structural issues.

Even RGGI States Now Admit There Is a Problem

Perhaps the most telling evidence that RGGI has drifted away from its original “no more than a few dollars per ton” promise is the RGGI states’ own recent language.

In the Auction 72 press release, the states tout the program’s benefits – emissions reductions, billions in proceeds, millions of households served – but then add a new note of concern: “Following this auction, the RGGI states intend to begin a scoping process to consider further targeted measures to continue to achieve reliable, clean electricity supply at affordable prices for consumers.”

Translation: at current prices and cap trajectories, the program is posing an affordability and reliability challenge serious enough to merit yet another multi‑year review process. This is the same program Acadia Center is selling to Virginians as an “energy affordability tool.”[3][2][1]

Given that the last program review, launched in late 2021, did not conclude until mid‑2025, there is a real risk that RGGI states will repeat the “slow walk” while allowance prices remain elevated and consumers bear the cost. If Virginia joins mid‑compliance‑period under these conditions, it will be volunteering its ratepayers to subsidize both regional climate ambitions and market participants’

Conclusion

The Acadia Report maintains that all is well with RGGI. I believe that its conclusions are not supportable. My analysis finds that RGGI now poses unacceptable affordability and reliability risks and needs immediate, fundamental revision. The RGGI states must disavow this report and acknowledge the enormity of the risks and engage regulators, system operators, and state lawmakers to consider substantive changes rather than the incremental tinkering contemplated in recent RGGI communications.